AI & RPA

Payments are moving to real time, regulations are tightening, and fraud typologies are evolving faster than rulesets. Traditional, siloed, rule-based transaction monitoring leads to high false positives, costly manual reviews and blind spots for emerging threats. A modern, AI-enabled and integrated approach across fraud, AML and sanctions is essential to deliver faster, more accurate decisions while maintaining regulatory compliance.

In our three-part series, Next Level Compliance: AI in Payments Transaction Monitoring and Financial Crime Prevention, we will examine the following topics:

Part 1: What is wrong with today’s transaction monitoring and how AI is transforming Anti-Money Laundering (AML), fraud prevention and sanctions and embargo screening.

Part 2: The regulatory implications for AI-based transaction monitoring.

Part 3: AI-driven business opportunities in financial crime prevention.

In this series, examples are drawn from Capco’s long-standing partner Hawk’s innovative platform to illustrate how artificial intelligence is redefining transaction monitoring and enabling financial institutions to stay ahead of emerging risks.1

Most institutions still run separate stacks and teams for fraud, AML and sanctions. Fraud and sanctions screening typically happen pre‑transaction while AML often triggers post‑event and reports to authorities (e.g. the Financial Intelligence Unit in Germany). Tools remain predominantly rule‑based: banks must pre‑define scenarios, which leads to poor detection of emerging patterns and a constant trade‑off between missing risk (false negatives) and overwhelming operations teams (false positives). As volumes grow, manual hit resolution becomes a cost and latency bottleneck, especially where timely approval or rejection is required. Legacy platforms also struggle with today’s data richness and quality demands. Even with standardization improvements (e.g. structured addresses), older systems often cannot scale or adapt to new payment rails and regulatory expectations, forcing institutions to consider modernization.

Schematic view of a transaction monitoring process

Instant payments (IP) eliminate the buffer for human intervention. Controls must operate inline, at millisecond latency, with high precision. Real‑time rails have proven more attractive targets for social‑engineering and account‑takeover fraud attempts. Experience from existing IP markets shows attacks rates are several times higher compared to those in traditional SEPA batch processing. In short, Instant Payments can mean instant fraud unless controls become both faster and smarter.

Historically, separating fraud from compliance was acceptable when decisions could be made after settlement. In a real‑time world, it is counterproductive. The same data, features, and analytic techniques—graph analysis, anomaly detection, and behavioral profiling—benefit all three domains. An integrated operating model reduces duplicated effort, aligns decisions, and improves risk coverage at the point of payment.

Data and features. Unified ingestion across payments, customer, device and external data, as well as entity resolution and risk‑relevant feature engineering enable models to learn behaviors, not just thresholds.

Real‑time detection. Machine‑learning and graph models score transactions in-flight, detect anomalies, and surface links across entities that static rules miss. Hybrid approaches retain business rules for hard constraints while letting models handle nuance and novelty.

Triage and case prioritization. AI reduces alert noise, ranks cases by expected risk, and generates investigator copilots to summarize context, freeing analysts to focus on true risk.

Continuous learning. Feedback loops from investigator decisions and regulatory outcomes adapt models as typologies change.

Where AI is less effective. Statutory checks with fixed logic (e.g. some list‑matching rules) and formal regulatory reporting formats remain best handled with deterministic controls as it is done currently.

Full platform swaps are disruptive. Many banks succeed with overlays that sit alongside and integrate seamlessly with existing monitoring and case‑management systems, adding real‑time scoring, alert optimization, and analyst tooling while legacy capabilities continue in parallel.2 Where deeper change is required, staged legacy modernization can de‑risk the journey by decoupling data, externalizing rules, and incrementally migrating use cases.

AI in compliance must be auditable. This means maintaining model governance (versioning, validation, drift monitoring), robust documentation, and human‑in‑the‑loop review for material decisions. Use explainability techniques to justify outcomes to internal audit and regulators. Align with regulatory expectations on data quality, fairness, and traceability. Integrate controls such as pre‑deployment testing, challenger models, performance SLAs and access controls.

Traditional AML monitoring relies on predefined scenarios that struggle with fast‑evolving laundering techniques. AI augments these controls by learning behavioral patterns across customers, accounts, and counterparties. Unsupervised anomaly detection spots deviations from typical behavior, while supervised models classify customer and transaction risk using historical outcomes. Graph-based network analysis surfaces hidden relationships and transaction chains that are indicative of layering and structuring. Institutions increasingly automate elements of suspicious activity reporting—from narrative drafting to data pre‑population—improving consistency and shortening turnaround times.

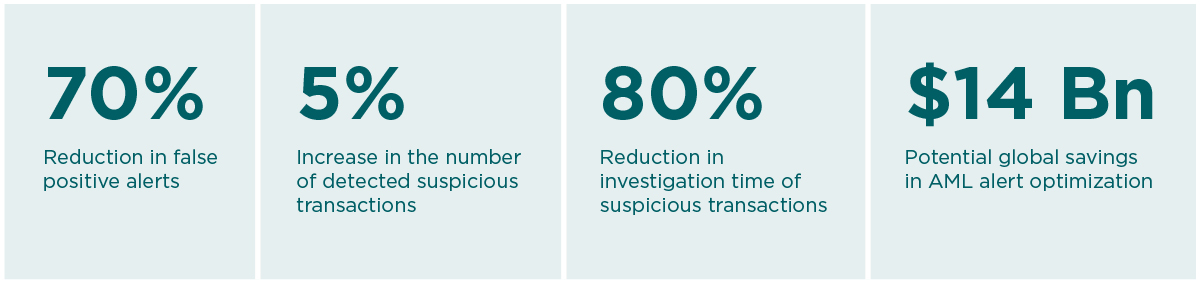

Benefits of applying AI to AML (source: The Global Treasurer)3

Fraud controls must operate in real time, especially on instant‑payment rails. Behavioral analytics build profiles at the user, device, and channel levels to detect anomalies such as unusual payees, amounts, or login patterns. Real‑time scoring classifies each transaction’s likelihood of fraud and triggers dynamic step-ups or holds when risk exceeds tolerance. Predictive models leverage historical fraud outcomes and near‑misses to anticipate emerging attack vectors, while feedback loops from investigators continuously refine thresholds and features to minimize customer friction.

Hawk’s real-time fraud analytics

AI strengthens list screening by improving fuzzy name matching and entity resolution—key for handling transliterations, nicknames, and incomplete data. Natural language processing models interpret context to reduce false positives from coincidental matches. Geospatial and routing checks add further confidence by assessing whether parties, banks, or payment routes intersect with sanctioned regions. Deterministic rules remain necessary for statutory requirements, while AI can focus on ambiguous, suspicious cases.

Effective AI in compliance depends on appropriate learning paradigms and high‑quality data. Supervised learning supports risk scoring and prioritization; unsupervised techniques discover unknown typologies and anomalies; and reinforcement learning can optimize sequential decisions in real‑time interventions. Representative examples include logistic regression and gradient‑boosted trees for classification, autoencoders and isolation forests for anomaly detection, and graph neural methods for relationship discovery. Training requires a unified data estate that combines transaction attributes, customer and counterparty profiles, device and channel signals, external watchlists, and adjudication labels. Robust data governance—lineage, quality controls, and privacy safeguards—is essential to ensure valid outputs and regulatory acceptance.

To meet the speed and complexity of modern payments, institutions must converge fraud, AML and sanctions into a single, AI‑enabled capability. Start by unifying data and features, introduce real‑time hybrid scoring and modernize incrementally through overlays or staged replacement. The result is fewer false positives, better detection of emerging risks and compliance that keeps pace with instant payments.

A pragmatic approach blends deterministic controls with AI‑driven analytics, governed by robust risk management models and clear documentation. Banks that unify these capabilities across AML, fraud and sanctions will achieve materially better detection at lower operational cost while preserving customer experience.

At Capco, we help financial institutions unlock the full potential of artificial intelligence to transform their transaction monitoring capabilities. With deep industry expertise and a proven track record in regulatory compliance, data strategy and technology implementation, we partner with clients to design and deploy AI-driven solutions that deliver tangible results.

We combine domain knowledge with advanced analytics and modern architecture to help organizations move beyond traditional rule-based systems. Our consultants work closely with clients to reimagine transaction monitoring frameworks, optimizing alert efficiency, reducing false positives and enabling faster, more accurate detection of suspicious activity.

Through strategic partnerships with innovative technology providers such as Hawk, Capco delivers end-to-end support, from AI model selection and data integration to governance, testing and regulatory alignment. The result is a scalable, explainable and future-proof monitoring ecosystem that not only meets compliance requirements but also creates operational and competitive advantage.

Whether you are looking to enhance your systems, modernize legacy systems or build a next-generation AI-powered transaction monitoring platform, Capco can guide you through every step of the journey, turning AI potential into real value.4 Contact us to find out more.

References

1 Capco and Hawk have been long-standing partners, bringing together Capco’s deep domain expertise in financial services with Hawk’s cutting-edge AI-driven transaction monitoring technology. This collaboration enables our clients to enhance their financial crime prevention frameworks, leveraging advanced analytics, machine learning and real-time anomaly detection.

2 For example, HAWK’s AML AI Overlay integrates seamlessly with existing transaction monitoring case systems, avoiding the need for a costly ‘rip and replace’ option when it comes to modernizing legacy systems.

3 https://www.theglobaltreasurer.com/

4 To find out more about Capco’s Legacy Modernization Toolkit, watch a short video here.