The FCA have signalled their intent through various initiatives to target areas where they think that customers are at significant risk of harm. These include their 14-point action plan to ensure that savings rates are being passed on appropriately, as well as the mortgage charter, intended to provide greater flexibility to those facing increasing mortgage repayments.

We have detailed areas where firms have found it challenging to implement the Duty’s specific requirements, and identified four key areas where focus and investment should be considered for delivery within Day 2.

1. Residual Day 1 Activity

Many firms have rightly focused efforts and resources on products and journeys where there is the greatest risk of customer harm, as well as on uplifting relevant frameworks and policies. Any residual review activity or outstanding activity for Day 1 should be carried out as an immediate priority.

Where firms have chosen to defer the fixing of identified customer harms to ‘business as usual’ status, they should ensure that a robust tracking process is in place to confirm that the fix for each item is completed, embedded, and evidenced.

2. Embedding Activity

The new control frameworks that were implemented during Day 1 will need further time and use to demonstrate full adoption. Enhanced product review processes, as an example, will require further work to acquire the necessary data and management information to substantiate assessments.

The compressed implementation period for Day 1 offered limited scope to provide deep and role specific training. Firms should now complete training based on a deeper understanding of the policy, and senior leaders should continue to take the opportunity to reinforce the policy by setting the tone from the top.

Customer Outcomes Testing and Monitoring should be utilised to validate the impact of newly established systems and controls, and to determine if there is a corresponding uplift in the quality of customer outcomes.

3. Back Book Review

The review of off sale products should be informed by the lessons gained from Day 1 activity. The metrics and criteria used to substantiate assessments of on sale products might not be the same for closed products but should be considered.

Firms must enter the closed book review with a plan for how to address thematic findings. Options should include changes to product characteristics, but firms should also consider their product simplification agenda to reduce the number of product variants that may complicate the review.

There is also a greater likelihood that firms will identify issues requiring redress, and these should be accrued for accordingly. We provide further insight on how firms should tackle the back book review here.

4. Capability Build

Firms should take this opportunity to invest in key capabilities within their business to enable more effective harm prevention while also enhancing the customer experience. This should extend into firms considering new innovative solutions to support this agenda.

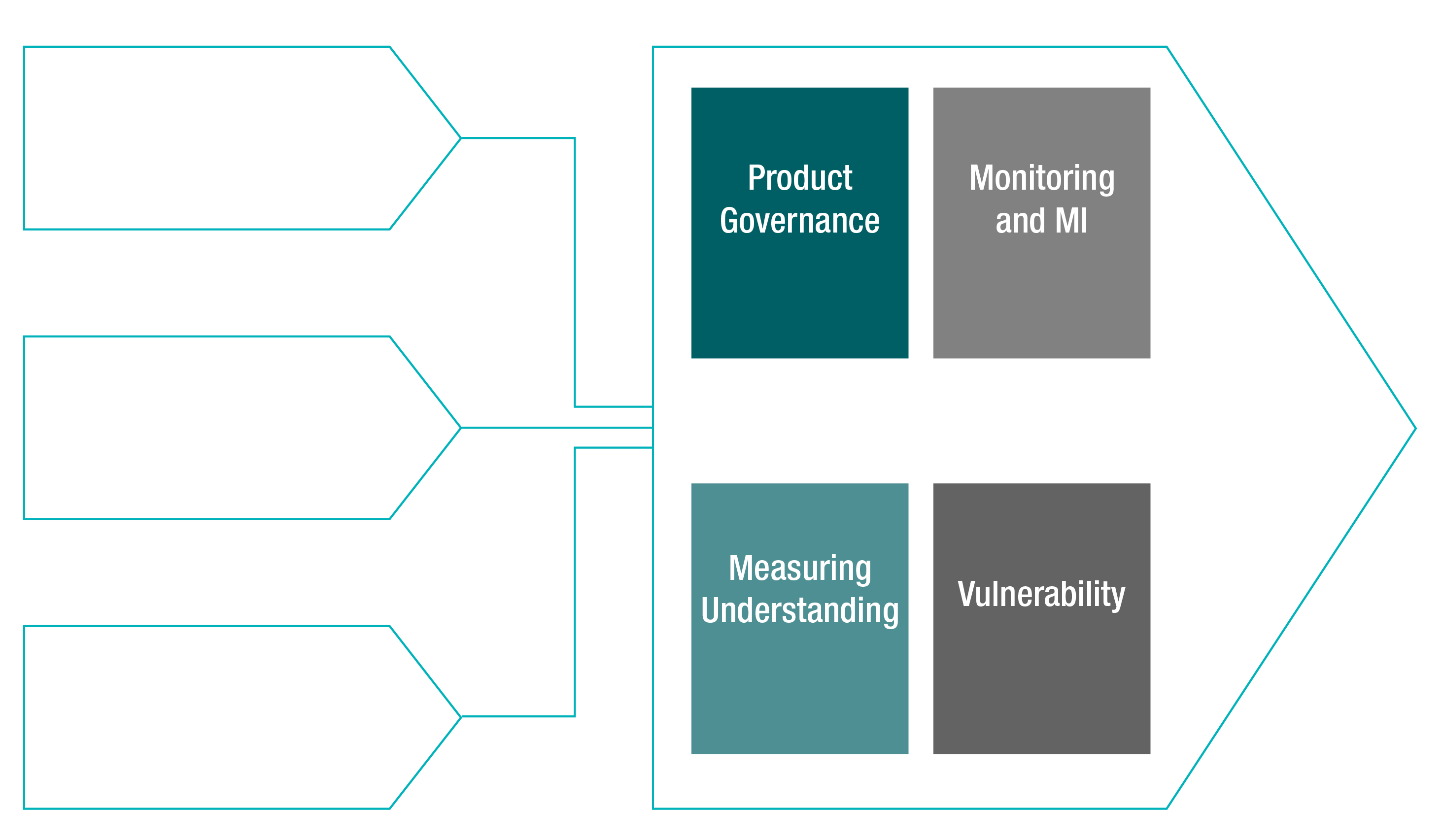

Fair Value and Target Market

Ongoing Monitoring, Management Information, and Board Assurance

Testing of Customer Understanding

Vulnerability