21 April 2020

COVID-19: COULD OUR NEW WAYS OF WORKING BECOME A NEW NORMAL?

In this blog, Harriet Scheiner explores how COVID-19 may change working life as we know it and shares how Capco are adapting to this ‘new normal’.

In the midst of the COVID-19 crisis, when many of us have had to implement continuity plans in a way we never expected, the Financial Conduct Authority (FCA) recently published a shortened business plan for 2020-21 on Tuesday 7 April. The plan focuses on both the short and medium-term objectives. The message is clear: the conduct agenda is not going away because of the pandemic.

Rather, the impacts of COVID-19 are putting extra focus on key topics.

In the short-term, the priorities that the FCA wants to ensure are:

Whilst the future of the economy is uncertain, it’s clear that the conduct agenda is here to stay. COVID-19 will likely increase the focus on long standing conduct challenges, including:

So how to prioritize? We believe businesses need to bring a more practical and integrated approach to managing the regulatory agenda.

Summary of business plan

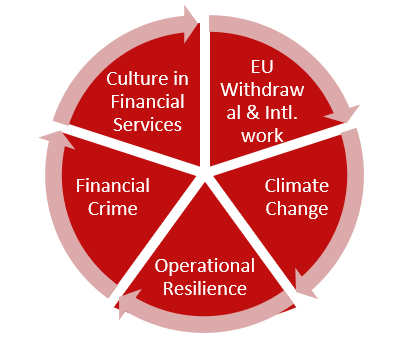

Cross-cutting and sector work:

As well as direct action to tackle COVID-19, the FCA have addressed five incremental areas which will have broader markets impacts on financial services over the next few years.

The FCA have also provided a summary for existing outcomes they are working to deliver across financial services which includes, wholesale financial markets; investment management; retail banking; and general insurance and protection (GI&P).

Objectives:

The FCA’s annual business plan is intended to explain strategic focus over the next three years. This plan will now be fundamentally reshaped by the impact of coronavirus on the UK and global financial markets.

Short term:

Focused efforts on ensuring:

Medium term:

Ensuring that consumers:

COVID-19 update:

To date, the FCA have already made a series of interventions at unprecedented speed to protect consumers, firms and the markets. This is to ensure that financial services businesses give people the support they need, that people don’t fall for scams, and that these businesses and markets know what we expect of them.

Actions thus far have been on the following objectives:

1. Keeping markets functioning and orderly during a major ‘repricing’ event;

2. Issuing emergency guidance so that government schemes can work;

3. Supporting consumers with the immediate shocks;

4. Keeping public access to essential banking services;

5. Protecting the most vulnerable in society.

The magnitude and duration of the economic shock resulting from this evolving situation is highly uncertain and negatively affects supply and the global economy, having not been like any economic downturn seen before identifying what is required to achieve a more stable position is the clear focus, measuring the impacts and size of the shocks presents challenges as it cannot be done quickly.

The FCA face difficulties planning ahead but the Business Plan sets out the key areas where work must be done to address the support required for firms and consumers. The situation is fast-moving and the FCA are responding on a daily basis and have already set out measures to help firms to support consumers and maintain orderly markets.

The enormous uncertainty about the size and nature of potential damage has made planning ahead much harder. The FCA have committed to keep plans updated in light of unfolding events, with their website remaining update regularly.

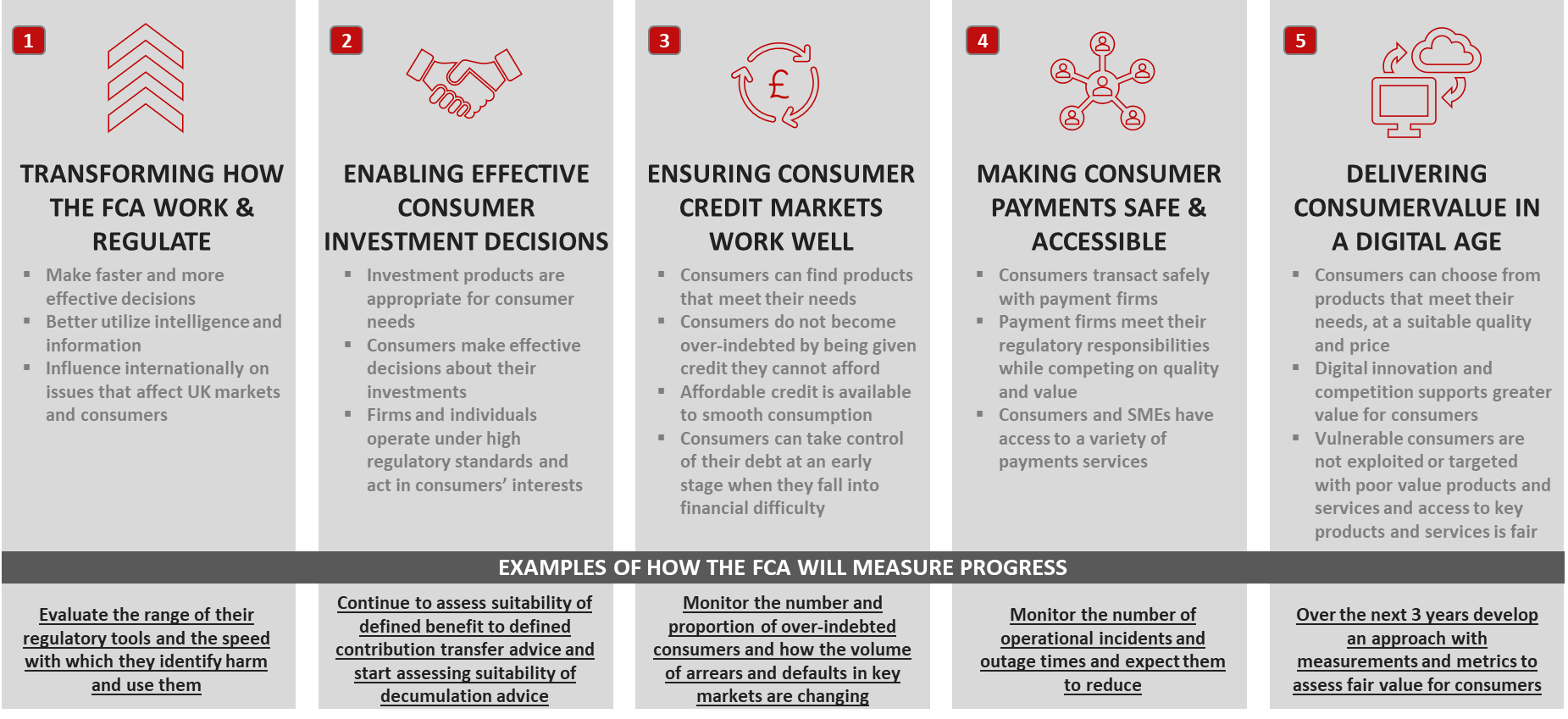

Key priorities for 2020/21:

The FCA has identified four external priorities to focus on over the next one to three years, the fifth priority being its own internal transformation. Progress on each of these priorities will be reported on in their Annual Report and Accounts 2020/21.

Based on regular dialogue with regulators and the industry, we believe there are three key steps all front office and compliance leads should be considering in working towards, for the best outcomes for customers and the organization:

1. Review current customer related outcomes against the FCA expectations

2. Ensure a COVID-19 related conduct plan is put in place

3. Review and prioritize overall regulatory book of work given budgetary constraints.

In actioning the above, build for the future, focus on the customer and have an open dialogue with regulators around the challenges faced.

If you want to find out more about Capco UK’s Regulatory offering, please reach out to the team below:

Richard Plumb, Compliance Practice Lead – Richard.Plumb@capco.com

Howard Taylor, Regulatory Delivery Specialist – Howard.Taylor@capco.com

Rebecca Howard, Remediation Specialist – Rebecca.Howard@capco.com