Americans’ consumer preference toward health-conscious products is increasingly causing wealth managers to re-examine their offerings through the lens of psychological and physical wellbeing. The start of the financial wellness trend began with retirement plan sponsors, such as employee benefits program, and is now accelerating with fintech firms.

Despite the growing popularity, studies show deficiencies across indicators. Many are unprepared for short-term shocks to their budgets or long-term financial goals. 40% of Americans express difficulty paying off an unexpected $400 expense,1 and economists found that following the COVID recession, 50% of workers over the age of 55 will be living on less than $20,000 a year or near that amount when they reach 65.2 Most concerning is that 60% of Americans reported experiencing stress over their finances.3 While these statistics are troubling, nearly every financial firm is aware of the trend and the potential opportunities it presents to transform financial wellness into a direct-to-consumer offering for the broader market.

While wealth management firms can offer personalized planning that covers financial wellness, consumers may not want all the other bundled investment products, tax, and/or legal services within the package. Innovative fintech firms will be rising threats for traditional wealth management firms challenging them to roll out capabilities and enhanced solutions to meet their consumers’ growing interest in financial wellness. Furthermore, the “great wealth transfer” from baby boomers to younger generations will push wealth firms to provide highly scalable personalized financial planning solutions to support incoming younger clients.

Connecting Advice

The most effective financial wellness solution will go beyond investment advice. This solution encompasses behavioral techniques to reinforce long-term financial health and habits. Consumers will be prepared for life events in advance, both planned and unplanned, through an easy-to-use digital platform. A well-executed strategy will keep consumers engaged in financial wellness to help achieve holistic advice. Wealth firms pursuing this endeavour will need to merge their wealth, banking, and insurance offerings to deliver holistic advice on the digital platform.

Today, financial products and services aim to solve siloed needs, such as investments tagged to specific goals, diversify portfolio risks, or debt reduction plans. Typically, they do not tie all the components together to offer a complete financial plan. While consumers may have access to thorough financial planning through a traditional advisor, they must sit through a full-blown financial planning process before advice is received. As a result, this makes planning non-modular in nature and tedious for the consumer. Rather, consumers should be able to access advice and solutions incrementally throughout the process, without sacrificing insightful and robust planning outputs.

Innovative digital capabilities, such as algorithms to solve for tradeoffs and data driven life planning, can help shift from a cumbersome planning processes to modular planning components. These components can be linked together for insights used to solve for unique and changing needs of consumers and provide holistic advice.

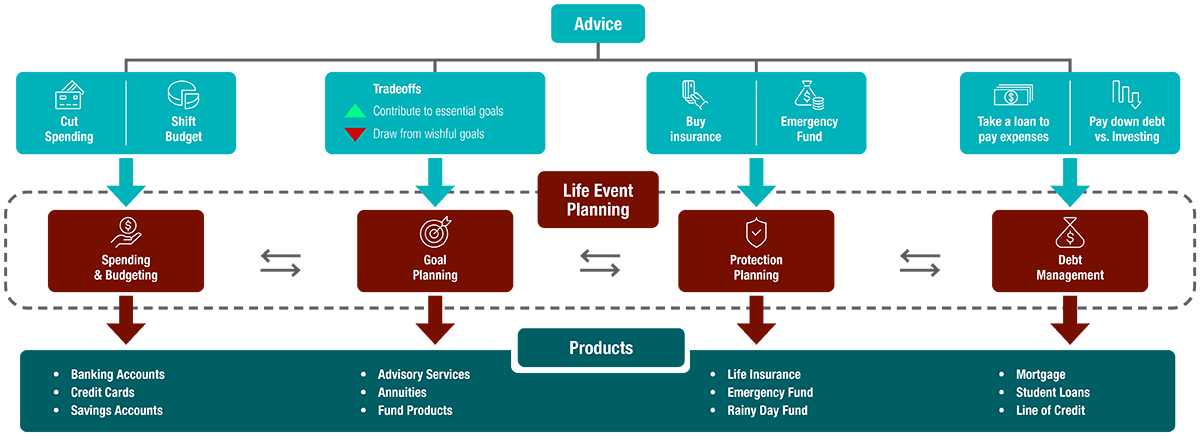

Holistic Financial Advice Framework: Four Key Pillars Connected by Life-Event Planning

Financial wellness contrasts with market-driven planning where products are recommended for client portfolios to prepare for market risks. Wealth managers focused on financial wellness can utilize socioeconomic data and life-event mechanisms to connect four pillars – goals-based planning, spending and budgeting, debt management, and protection. Products and services are then highly personalized to the advice generated. The future of wealth management would lead with advice rather than products. Examples below:

• Can I afford a house/car/boat? Planning monthly payments for big-ticket goals in the context of an overall budget helps achieve the goal comfortably with minimal effect on daily life.

• How will I support a newborn? Tradeoffs can be achieved for spending and budgeting adjustments, medical expenses for the newborn, and medical and life insurance protection.

Life-event planning will be driven by what-if analysis connected with data across the four pillars. In essence, participants can view a snapshot of their financial wellness, as well as obtain holistic advice.

Evolution of Advice

Wealth management firms offering products without completely understanding needs of an individual will be an outdated model to properly serving clients. Firms must be able to contextualize advice to events tying it to the four pillars in which products can be suggested as vehicles to implement financial solutions.

By this process, clients can improve financial literacy, identify negative financial behaviours, and reach overall financial wellness targets. Building a foundational financial wellness program will require research and design to differentiate experience, thereby guiding institutions and wealth managers in delivering products that are truly holistic, personalized, and effective to clients.

________________________________________________________

1. The Federal Reserve (2019). Report on the Economic Well-Being of U.S. Households in 2018.

2. MarketWatch (2020). Opinion: Half of Americans Over 55 May Retire Poor. https://www.marketwatch.com/story/half-of-americans-over-55-may-retire-poor-2020-10-01#:~:text=In%20an%20interview%2C%20economist%20Teresa,in%20poverty%20or%20near%20poverty.

3. American Psychological Association (2019). Stress in America: Stress and Current Events. Stress in America™ Survey.