Across the world, the digital revolution is transforming customer expectations and disrupting key markets, including financial services. Banks in the Middle East are responding by scaling up their digital innovation and trying to adopt relevant fintech behaviors, for example in terms of rapidly launching new digital products and hyper-personalizing their offerings. However, the core processes of many incumbent banks are based on technologies more than 25 years old, and the burden of legacy core technology has become a critical limitation on bank agility and the scale and rate of industry evolution.

Banks in the Middle East have launched important initiatives to modernize main bank core processes, but there is a growing realization that progress must be faster, more transformational, and deliver greater openness and flexibility. That effort will prove critical to building new personalized services for the region’s youthful, mobile-oriented consumers, and to supporting Middle Eastern economies as they diversify out of carbon-dependent, commodity-driven industries into more sustainable, services-based economies.

In this white paper, we identify the drivers of core transformation within a Middle Eastern context, set out the key barriers to change, and explore how to overcome these using a three-pillar approach to successful transformation.

FOUR KEY DRIVERS OF CORE BANKING TRANSFORMATIONS IN THE MIDDLE EAST

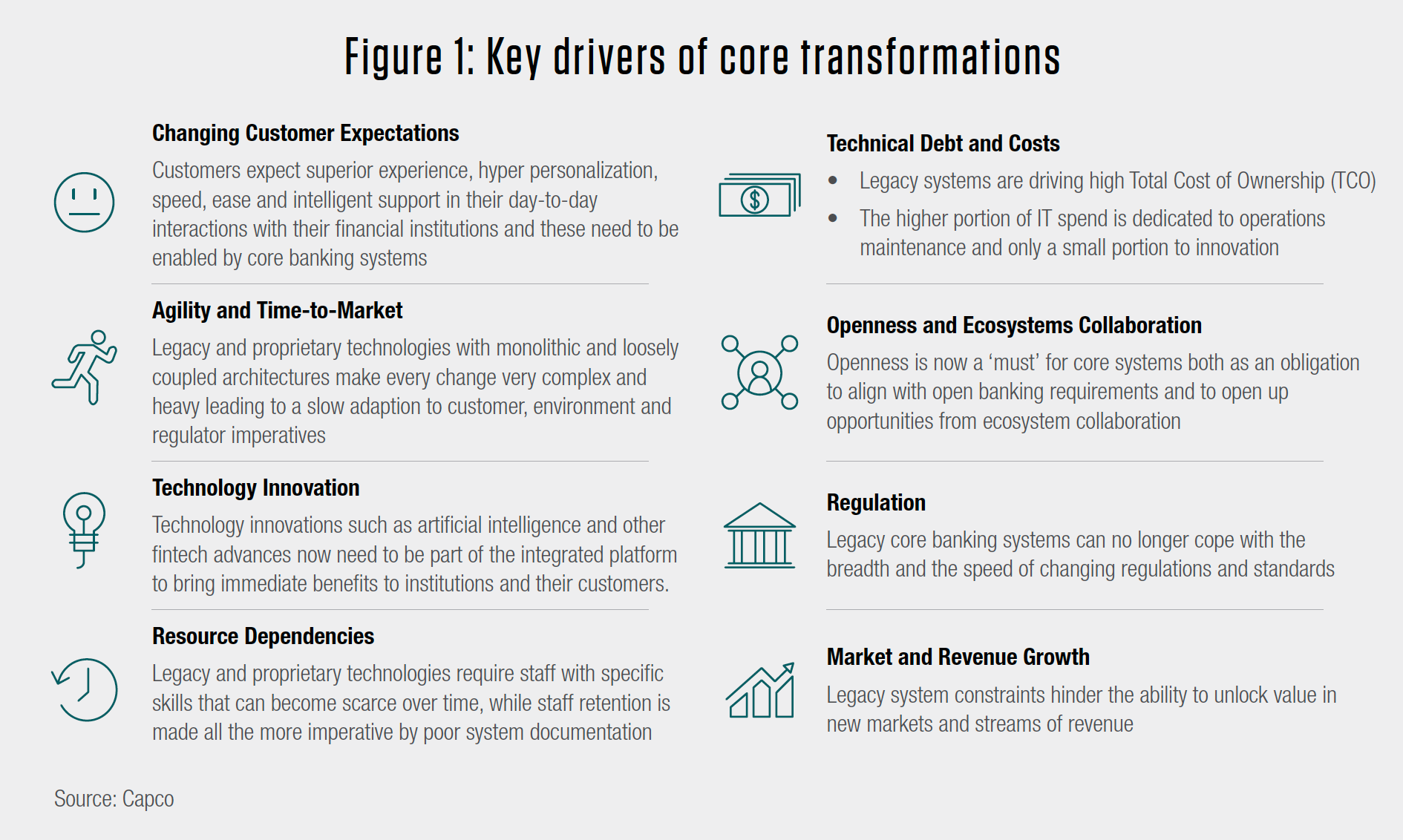

The key drivers of core banking transformations are well understood at the global level (Figure 1), and while all are relevant in the Middle East, four have a particular resonance.

The first of these is the rapid rate of changing customer expectations. The Middle East is characterized by young, digitally savvy banking customers, with high rates of personal consumption. These customers now expect easy, convenient hassle-free digital customer journeys in their daily lives and banking services. They do not want, for example, to have to shift to another app to spend the rewards they have accumulated on their credit card, or to fill in multiple applications when purchasing cross-sold products. However, answering these needs requires a modern core that can integrate easily with, and supply real-time information to, the hyper-personalized, real-time embedded banking services of the near future.

Core transformations are not something that banks willingly do twice, so learning from experience is not an option.

Increasing competition in Middle Eastern banking markets – including challenges from fintechs, greenfield digital-first banks, and potentially ‘Big Techs’ – means that banks need to rapidly build and launch new services through improved agility and time to market. This second driver explains the new trend towards ‘composable banking’, which applies microservices and API-first architectures to improve the granularity and connectivity of banking core systems, their functions and key associated applications. With the right architecture, each discrete bank function can be reused to speedily build new products, while other functions can be supplied or augmented through easy-to-integrate ecosystems of external vendors. The new core architecture can then support a wider culture of innovation across the bank and unlock profitability through scalable operations.

The third regional driver is the role of technology innovation across Middle Eastern economies. The market research company IDC forecasts that digital transformation investment across all industries in the Middle East, Turkey and Africa region will more than double in the 2021-2026 period, as CIOs double-down on a digital-first future after the pandemic. The trend is related to a host of national campaigns such as the UAE’s various strategies to become a global center of the digital world and its Financial Infrastructure Transformation Programme (FIT), or Saudi Arabia’s Vision 2030 and Financial Sector Development Program. In this broader economic and political environment, Middle Eastern banks are aware that their core infrastructure needs to be ready to:

Neither objective may be attainable while massive technical debt forces bank technology teams to maintain and adapt obsolete technology, rather than working on innovation and strategic improvements. The scale of technical debt in Middle Eastern banking is also creating significant resource dependencies, our fourth key regional driver. As the legacy coding skills required to maintain legacy systems become scarcer over time, the reliance of Middle Eastern banks on a large ex-pat workforce is making them particularly vulnerable. The region’s banks need to move to core technologies that require far less maintenance and that, through composable banking and low- and no-code approaches, shift day-to-day workloads towards business lines and wider ecosystems rather than central technology teams.

THREE PILLARS OF SUCCESSFUL TRANSFORMATION

The drivers of core transformation in the Middle East are compelling and the region’s banking industry seems prepared to invest in its long-term goal: lean, agile, cloud- and microservices-oriented architectures around the books of record.

For many banks, however, the barriers to transformation remain daunting, including fear of failure given the banking industry’s patchy record of core transformations; a desire to avoid ‘Big Bang’ risks during core data migration to a new system; concern that regulators will not yet accept moving data to new cloud-based solutions; uncertainties about how to select the right technology strategy; and a lack of experience in how to set up and govern such large, bank-critical multi-year programs.

Some of these barriers are weakening. For example, as global cloud-providers move to establish data centers in the Middle East, regulators are cautiously opening discussions about a more cloud-based future for banking. However, the most important challenges are ‘internal’, in terms of setting the right goals and road map and deploying resources in the right way.

Capco has gained significant experience in the UK and around the world in planning and implementing bank core modernization and transformation strategies, as well as in setting up digital-first neo banks. Our tried and trusted approaches suggest that banks in the Middle East can significantly increase their chances of success by strengthening three pillars of core transformation: the case for change, strategy selection, and execution planning.

Change management is an even bigger factor than technology selection in determining success. Failures in core banking transformation can often be attributed to underestimating the significant effort and cost, the need for leadership support, and the importance of robust planning and governance.

1: The case for change – Clarity around bank-specific goals

Core transformation affects the whole bank, can take three or more years, and involves a considerable investment in terms of the dollar figure and allocation of talent. Banks easily lose their way during this multi-stage, multi-year exercise and begin to question why they have embarked on it – which can lead to the sacrifice of long-term benefits for short-term expediency.

It is therefore essential to clarify the business case for change in terms of overall objectives and guiding principles at the outset, so that these can act as the bank’s North Star during the initial discovery process and throughout the transformation. Some fundamental observations:

2: Strategy selection – Getting to your target state from where you are now

To avoid setting off in the wrong direction, the bank needs to understand where it is now as well as where it is going. The discovery phase must therefore include a current state definition (including key business pain points) that can be compared to a detailed target state (defined by the bank’s case for change).

It is essential to clarify the case for change so that it can act as the bank's North Star during the shaping phase and throughout the transformation execution, while balancing this with the flexibility to accommodate changes and the agility to unlock more value.

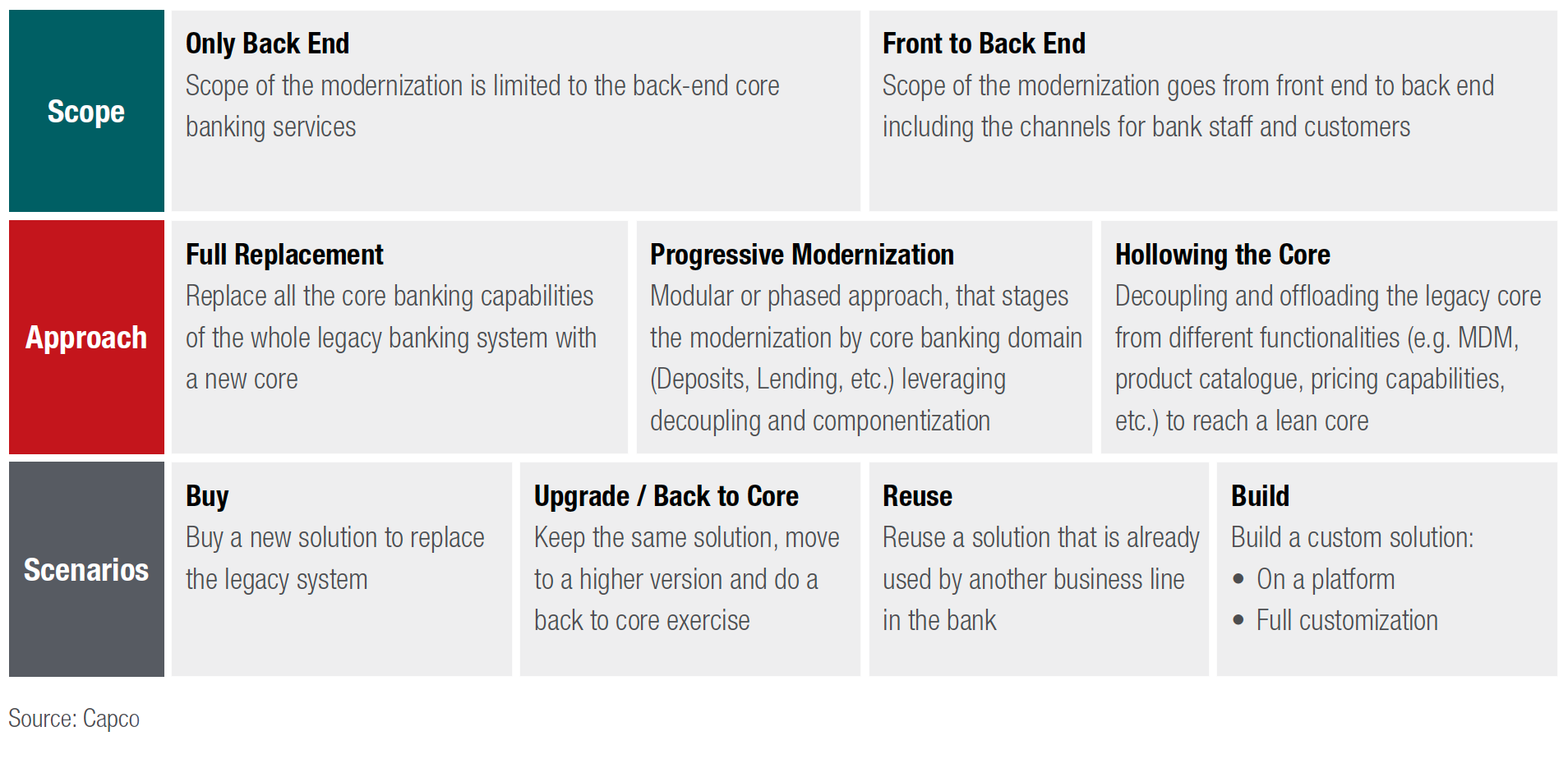

Based on this gap analysis, the bank must select a strategy and useful transitional stages that comprise the optimal route towards the target state. Strategy selection should include exploring a set of modernization options, set out in Table 2 at a high level, and the key technologies that support these. Some observations:

Figure 2: Strategy selection: Core banking modernization options

3: Execution planning – Route maps and governance frameworks

Like travelers setting off on a long journey, banks must plot out a route map that has a clear destination while remaining flexible enough to accommodate changes in customer requirements and advances in available technologies. The route map should be supported by an execution and mobilization plan that sets out the resources the bank will need, such as a right-sized core transformation team and a governance framework to ensure that the project remains on course. Some observations:

CONCLUSION – PLANNING FOR SUCCESS

Banks in the Middle East are at the center of the region’s shift towards digital, services-based economies. However, many still depend upon legacy core technologies that will restrict their agility in terms of launching innovative, hyper-personalized, data-driven products and services.

Banks have been reticent about launching core transformation projects because of the complexity and the risk. A series of strategies and technologies that can reduce the risks of core transformation are being tested in the global marketplace, but they all have pros and cons. Banks must identify which will best address their present situation, internal capabilities, risk appetite and key ambitions.

Accelerating digital disruption means banks need to take decisions on core transformation. However, pushing forward without properly defining where they are now and where they want to go could set banks on the wrong path. In this paper, we’ve argued that the answer is to fully develop the bank’s case for change, use this to consider the range of strategies and technologies that are becoming available, and then build an execution and governance roadmap that delivers value early on. For banks in the Middle East, this offers a route to core transformations that can foster step changes in innovation, the ongoing disruption of local markets, and the capture of global opportunities.

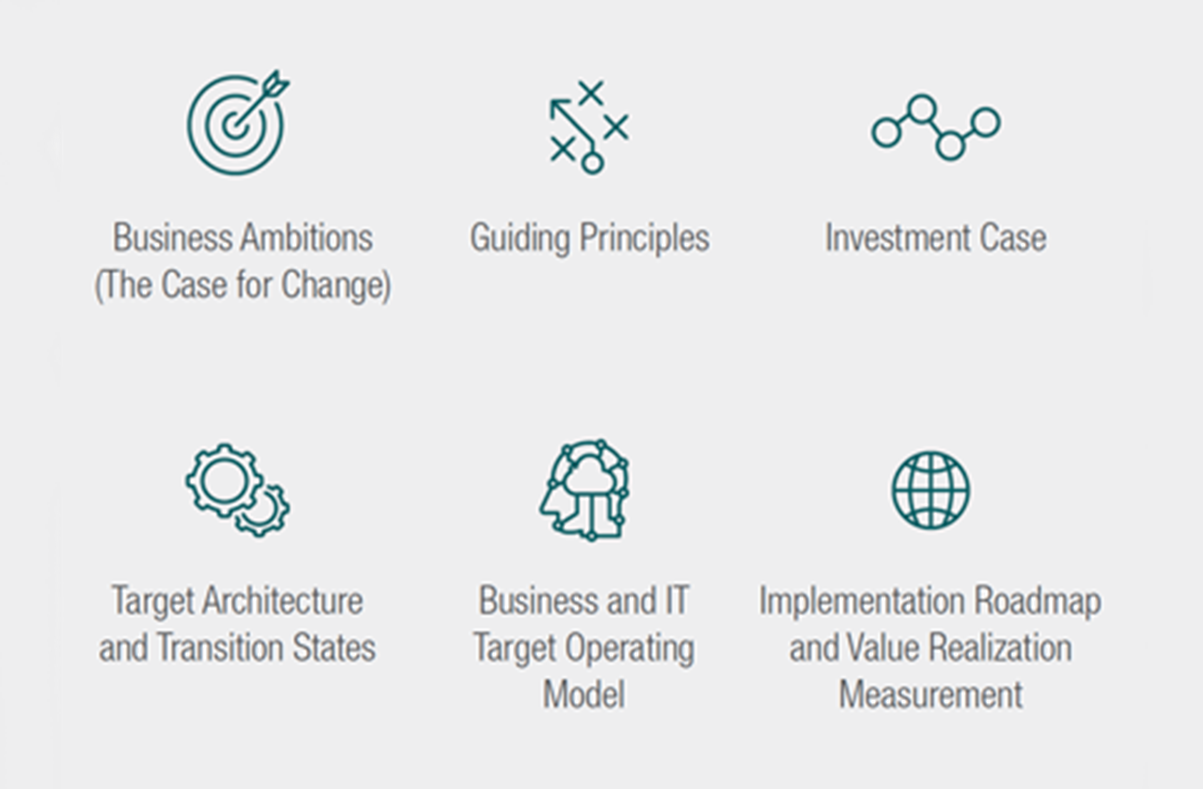

Figure 3: Next steps: What tools do you need to minimize risk and maximize benefits?

AUTHORS

Naim Alame, Managing Partner, Capco

Kushal Dhammi, Managing Principal, Capco

CONTRIBUTORS

Alex Ross-Wilson

Andy McGinn

Kane Stavens

CONTACT

Naim Alame, Managing Partner, Capco