A shift in market landscape is forcing financial institutions to adapt to the new needs of a growing client segment. Firms that strategically develop an integrated offering for this next generation of clients will see a surge in growth, while those who lag risk losing their market position.

Client demand is changing – 49% of today’s wealthy clients would prefer a single financial institution to serve most of their financial needs. What’s interesting is that only one-third of clients are behaving in this manner. Why? Because not all firms have the capabilities in place to satisfy the diverse needs of their clients.

Financial institutions are under a tremendous amount of pressure to adapt and innovate to fulfil everchanging client preferences and capture a larger market share. Fintechs, such as Stash, Chime, and many others, are creating innovative solutions that combine traditionally siloed banking and wealth offerings into an innovative, integrated solution. Their approach targets younger customers earlier in their financial journey and provides them with products and services that meet their needs each step of the way. Traditional banks, on the other hand, are falling behind – leaving money and opportunity on the table. These incumbent firms are experiencing a major push to gain a larger market share in the wake of Fintech disruption and need to act now to remain competitive.

There is a gap between client interest and firm execution, which presents a major opportunity for both wealth managers and banks to consolidate existing client assets. Traditional banks are investing in wealth management capabilities and traditional wealth managers are now offering new banking services. This is evidenced by Charles Schwab offering wealth management customers checking accounts, and Goldman Sachs rolling out Marcus – a suite of financial tools to help clients grow and manage money. Although these firms are doing it successfully, many firms fail because these offerings fall flat without targeting the right audience.

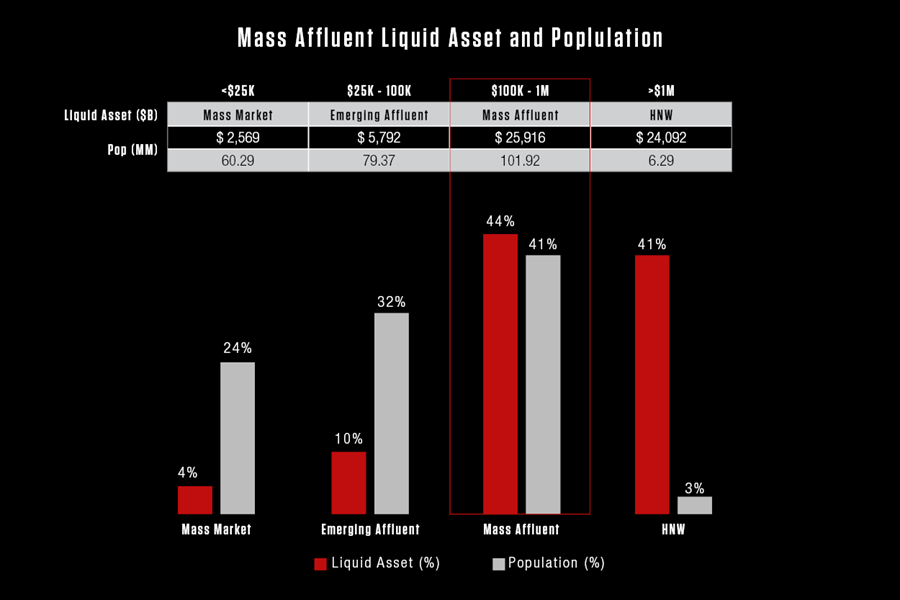

The target customer for this convergence sits within the banks’ existing customer base – the mass affluent segment. This segment represents the largest wealth segment in the U.S., both in terms of liquid assets and population. It is a ripe target – made up of future customers given the aging client base and pending wealth transfer. Furthermore, they make up a large percentage of customers for traditional banks to cross-sell wealth. The mass affluent segment is often inadequately served in comparison to other wealth segments – most firms provide extensive private and retail bank products and services available to cater to the high net worth and mass market segments, respectively. Since this segment is both stable and quite large in comparison to other market segments within the banking and wealth industries, firms are faced with the key decision of how to position themselves to stay competitive to best serve this demographic.

To be successful in attracting the mass affluent market, traditional firms must carefully define the experience needed to attract this segment across banking and wealth. One key need of the mass affluent segment stems from their rapid adoption of digital-first channels and self-service capabilities. With the rise in popularity of Fintech companies, such as Robinhood, and the various wealth capabilities they offer lower market segments, the mass affluent segment expects firms to offer personalized solutions and unique insights to see the value in their services. Financial planning tools are key – planning, coaching, spending, and saving are top drivers of financial activity for this segment. Mass affluent clients respond to incentives to bring about a holistic relationship – for example, providing better rates on mortgages if you have a certain threshold in AUM with the bank. Additionally, this segment values a single view of their holistic financial situation, with technology touchpoints providing data-backed advice on how their assets should be managed. If a firm wants to be successful in attracting clients in this market, these key considerations need to be cemented into its digital strategy.

To successfully capture the mass affluent market, firms need to break down organizational silos that traditionally make this convergence difficult. A new approach is needed to successfully cross-sell banking and wealth products to mass affluent clients. Today, most retail banks can only cross-sell <1% of the population, missing the opportunity to meet clients’ growing demands for wealth advice. Banks offer a suite of products and services but fail to highlight the key benefits for client goals.Fintechs, on the other hand, have succeeded in bridging the gap between client goals and unique products and services, but they lack the personalized touch traditional banks have for their clients. To be successful, banks need to adjust their products and services to be highly personable to their client goals. A recent successful example of this is Bank of America offering Life Plan to bolster its Merrill Wealth offering to its existing bank customers – an integration that provides a personalized digital experience to help clients achieve their most important goals.

With ample resources in the market, there isn’t a need to reinvent the wheel. Banking firms, now, can leverage capabilities of wealth partners (and vice-versa with wealth firms leveraging the capability of their banking partners) to create functional ecosystem that delivers value to their clients. This is evidenced by Morgan Stanley merging with ETRADE, where Morgan Stanley aims to cross sell banking products via ETRADE and expand their offerings.

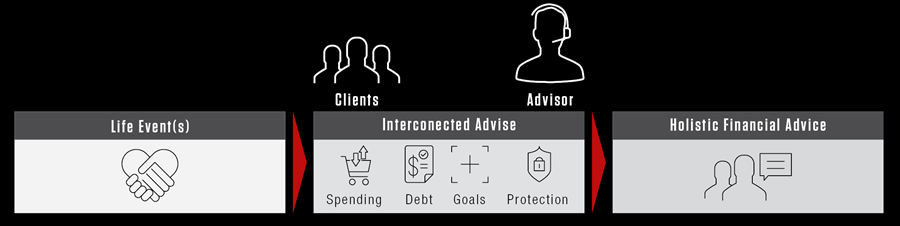

Firms need to start with the low-hanging fruit and not take on everything at once – instead of pushing a catalogue of products for customers to choose from, firms need to lead with advice, powered by unique capabilities, products, and solutions. First, a goals-based planning experience generates proactive, bespoke triggers that may pique a customer’s interest. Then, advisors, who deeply understand a firm’s capabilities and products, provide actionable advice on how to help customers reach their goal. In other words, to deliver holistic advice to a client, banks need first to understand what the client wants to achieve.

In order to achieve this, it’s important for financial institutions to define their vision, develop a compelling value proposition, and validate the economic opportunity and business case, with a major focus on how to create a digital experience that speaks to mass affluent clients. The right choices on an implementable roadmap will bring the strategy to life through executable features and capabilities.

Contact us to learn more:

Isaac Halpern, Head of Strategy, Isaac.Halpern@capco.com

Nikhil Sharma, Head of US Digital Wealth Management, Nikhil.Sharma@capco.com

Carl Repoli, Capco Strategy, Carl.Repoli@capco.com

1https://www.wealthmanagement.com/industry/clients-want-one-stop-shop-banking-cerulli-report