Using NFTs as collateral streamlines the lending process by creating collateral that,

despite its high volatility, reduces counterparty risk and provides capital efficiencies for trade participants by accelerating clearing and settlement to real-time.

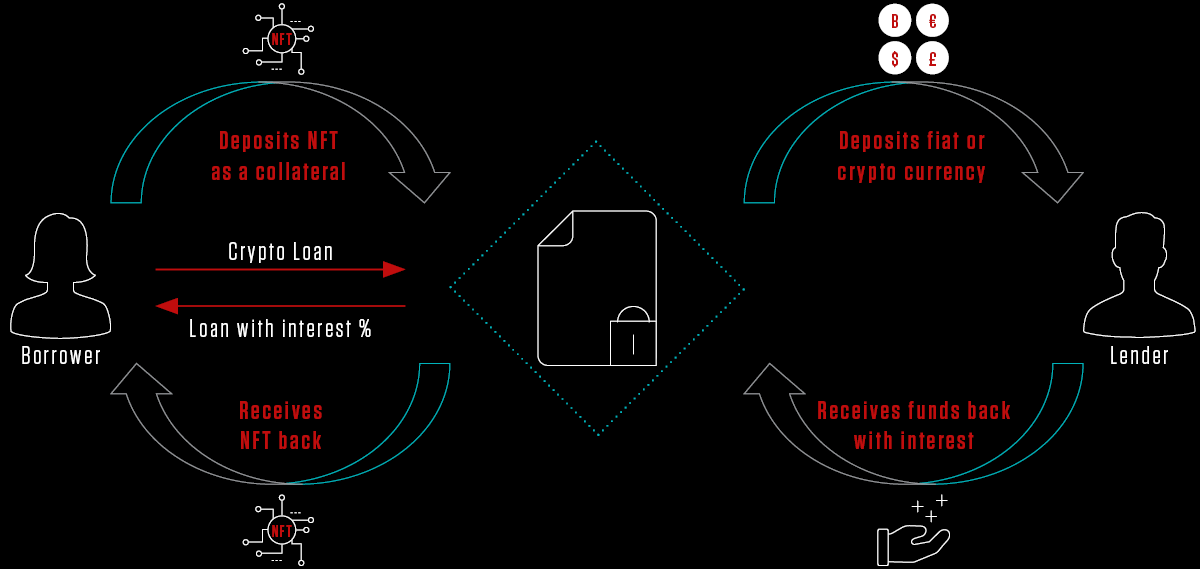

Non-fungible tokens have risen in price in many collections and have returned to the public attention, hitting $25 billion in sales in 2021 . As virtual reality evolves and blockchain becomes more widespread, projects like the Metaverse will soon take on a new shape, supported by various NFT projects. However, the bond market is an important missing factor in the NFT ecosystem. Most NFT users use their NFTs only when playing certain games or interacting with certain platforms. Unlike alternative cryptocurrencies, you cannot stake all NFTs. However, various marketplaces for NFT-backed loans allow borrowers to put up assets for loans, while lenders can make offers to lend in return for interest. A typical transaction comprises the following steps:

Many NFTs on the market are relatively illiquid, and various decentralized finance studies have detected a rising need to increase NFT liquidity, creating an opportunity for banks and on the other hand presenting new opportunities for collectors to leverage their NFTs beyond the passive buy-and-hold option.

Since NFTs have different prices and people are willing to pay different amounts for the same thing, the price determination is not easy. To determine the fair value of NFTs, banks could establish a marketplace where NFT owners mortgage their NFT pieces or collections in exchange for crypto or fiat currencies.

Once both parties agree on the terms, the NFT would be deposited from the borrower's wallet into an escrow account managed by the bank, and the loan could be facilitated through a smart contract. By providing a secure marketplace for NFT owners and utilizing their NFTs as collateral, banks could support collectors and investors in a variety of ways, including boosting liquidity and supporting fair pricing for NFTs, thus increasing portfolio variety and opening a new market of NFTs.

This allows banks to benefit from decentralized ledger technology (DLT) while also increasing their top and bottom lines by introducing a new product category, namely, collateralizing digital assets and profiting from the spread and transaction fees. Introducing NFT use cases will also help the bank stay ahead of fintechs and other competitors while additionally helping develop their business strategy.

Digital assets are becoming increasingly interesting as an asset class for institutional investors. We believe that increased service/product offerings by institutional investors will further drive significant investment interest over the next few years. Banks can use the early-stage exposure opportunity now to position themselves for competitive advantage over other market participants.

Capco combines innovative thinking with extensive expertise in digital transformation to create the greatest possible value for clients. We support clients in setting up their digital asset strategy as well as embedding the required technology into legacy systems.

To find out how we can help you with your digital asset strategy or to learn more about DTL and crypto and how your firm can benefit, please contact us.