How to reshape your customer strategy to ensure protection and support across the board.

In our previous blog post, COVID-19 and Financial Institutions: March was a Dress Rehearsal, we discussed the current situation and how financial institutions have been more reactive than proactive in this crisis. Within this blog, we outline the four pillar pandemic customer strategy Capco has developed to help banks continue to support customers in distress. Financial institutions need a comprehensive channel response that will span across all customer segments as they feel the impact at different stages of the crisis (cross-channel coordinated customer engagement).

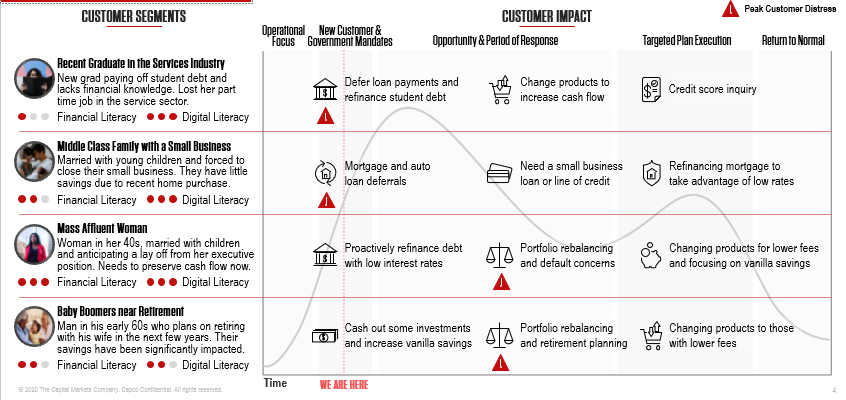

In the illustration below, we see that different customer segments have very different short-and-long-term financial priorities. Combined with varying levels of financial and digital literacy, it is clear that financial institutions cannot apply the same approach across all customer segments. A pandemic customer strategy is the first step towards being able to identify the different product and service needs of customers, and also provide them at the time when customers most need them most.

Financial institutions need to be prepared to provide this support over an extended time through various channels and means. Additionally, they should start to identify the customers who will soon be in distress proactively. For instance, the younger generation with less job security and who may be more impacted by the recent shut-downs will likely need immediate assistance. Although they have a higher digital fluency, they may not be as financially savvy and will need help navigating the next couple of months.

For others with more financial means to help carry them through the crisis, the priority will be to start preserving cash flow should job cuts come down the road. The banks will have a unique opportunity to proactively identify these customers before they hit their most distressing point. The customers closer to retirement, especially those who struggle with digital literacy, will need focused support in navigating the preservation of their savings, rebalancing their portfolios, and potentially recouping losses.

The window of opportunity to help customers depends on their potential points of distress. How can financial institutions build and execute their pandemic customer strategy without dropping the ball when customers need them most?

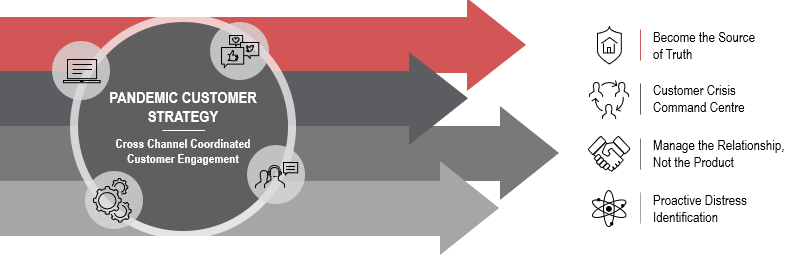

Capco has identified four pillars as the keys to a successful pandemic customer strategy:

1. Financial institutions should become the source of truth for their customers. Be the one-stop-shop for everything customers need to figure out what supports are available to them and how to access them or apply. To become this trusted source of truth, they need:

The responsibility of locating information should not fall on the customer.

2. To emphasize the role of the one source of truth, banks need to maintain customer crisis command centers that will solely focus on these proactive communications, curating a singular voice for all digital and social media communication. Financial institutions need to develop crisis management protocols for both digital and assisted channels to ensure customer support is consistent. The command center will also be proactive in its development and sharing of new customer interactive crisis management tools.

3. Financial institutions are in a unique position to help mitigate the economic impacts of the pandemic for their customers. They will only be able to do that by developing and offering tools and products that focus on the overall customer relationship. For example, loan deferral fraud rules and applications that consider the customer’s entire relationship with the bank, and not just on a product by product basis. This relationship focus needs to be prioritized and maintained throughout the next year. It will define how banks interact with customers going forward, not just over the next 12 months but into the foreseeable future.

4. Artificial intelligence capabilities should be employed to build models that will identify customer actions/behaviors to indicate upcoming distress. Once they develop these modeling capabilities, institutions will be able to identify customers likely to require assistance, proactively provide support before that customer hits the moment of crisis, and hopefully avert said crisis.

The next few weeks should focus on easing financial tension and uncertainty, establishing clear communication channels, and forecasting future distress indicators. From there, financial institutions should focus on enhancing digital capabilities and integrating with assisted channels and product operations to support customers during these uncertain times proactively. If the banks can implement a strategy similar to the four-pillar approach outlined above, they will not only be able to mitigate their own risk, but also protect and support their customers, which in turn is likely to assure the longevity of the business.

To learn more about how Capco can help you and your business develop a comprehensive channel response and be better positioned to adapt to this changing cultural and financial landscape, please contact us kam.gill@capco.com.