European history suggests that the Commodity Murabaha may have a wider appeal and application beyond Islamic Finance – notably to address the ongoing aversion to usury among practitioners of the Catholic faith.

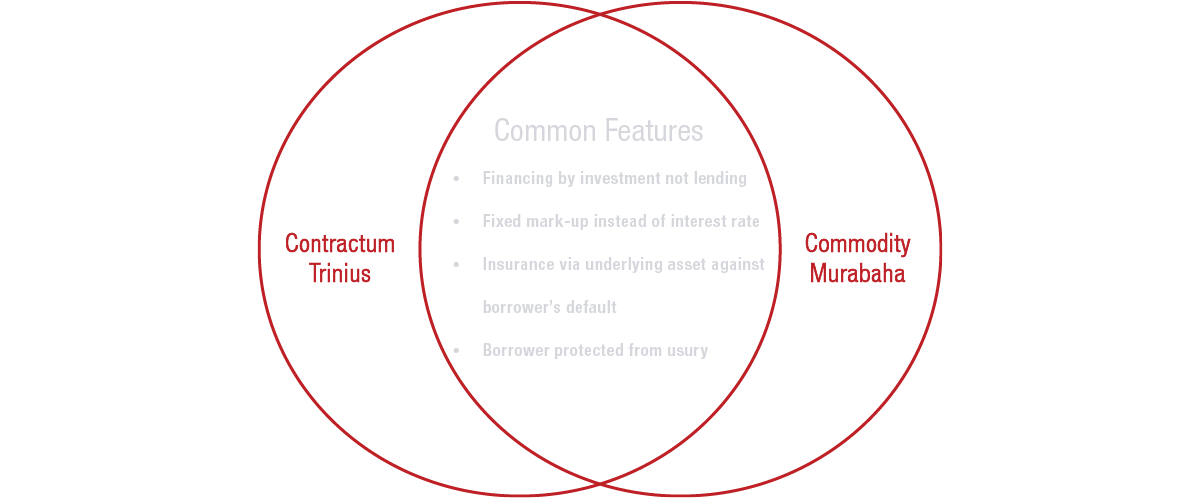

The Islamic faith’s prohibition of usury – riba – rules out the use of bank loans or the application of interest. For that reason, Shariah-compliant asset financing – Murabaha, essentially a cost-plus form of financing – sees the seller and buyer agree in advance on the cost and mark-up of an asset1. In the case of the Commodity Murabaha, the transaction agreement is based on the purchase and sale of a commodity, often a base metal such as tin or iron.

Less well understood is that, going back in history to when the vast majority of Europe was Catholic, the practice of charging interest was similarly forbidden by the Roman Catholic Church. The Contractum trinius was accordingly devised by medieval bankers to replicate a fixed-interest loan by way of three simultaneous transactions: an investment by the lender in the borrower’s goods was combined with a profit-share arrangement in exchange for a fee, as well as an insurance contract between the two parties2.

Today, while most people across traditionally Christian countries do not question the structure of the loans they take out, the idea of interest as being unethical persists among Catholic communities. John Finnis, a former Professor of Law & Legal Philosophy at the University of Oxford, a prominent contemporary philosopher and a widely-referenced Catholic scholar, has written that “to make any further charge in respect of the loan of money is unjust, and the name for this sort of charge – this sort of wrong – is usury.”

This suggests a role for the Commodity Murabaha, which stands as the closest financing structure to the previously mentioned Contractum trinius, as illustrated in the diagram below:

One example of effective Islamic Finance (IF) structures can be seen in the home finance space. Islamic banks and other non-traditional IF players offer a co-ownership scheme partnership agreement whereby the buyer and the bank can purchase a home together. The home buyer would then purchase shares in the property over a period of time, while paying rent. Depending on the equity ownership the rent can be scaled down. As this is not a debt-based partnership, contracts can be flexible. This includes risk sharing and is a rent-to-own type product which avoids the exposure to interest rates.

Co-ownership or Commodity Murabaha could in theory offer a very welcoming financing solution in the less mature markets where many borrowers are exposed to a disproportionate risk due to an insufficient provision of fixed interest rate loans. Borrowers in Central Eastern European countries such as Poland – where almost exclusively it is variable interest rate loans that are available1 – would certainly benefit from insulating themselves from today’s rising interest rates by way of a modern-day version of a Contractum trinius. Such loans were the default option for Polish borrowers, but the structure of the loans has proved extremely problematic due to their denomination in or indexing to foreign currencies (notably Swiss Franc)2.

Such issues would have been avoided if Commodity Murabaha had been used instead, as the financing structure would not have allowed for any rate of interest, let alone a floating one, or any derivatives, including FX options. Importantly, the Islamic banking and finance in most countries operates under the principle of fractional reserve3, just like the traditional European and American banks do, and as such the Commodity Murabaha products are also financed in the way that traditional mortgages and loans are financed by the banks. Therefore, the banks could in theory offer IF products alongside their traditional mortgages and loans.

Furthermore, this asset-backed finance mechanism would appeal to ESG/socially responsible investors and provide a faith-based alternative to those who seek an alternative, including SMEs that make a positive contribution to society.

The Murabaha structure could also be applied to a wider variation of products, ranging from those resembling a Contractum trinius – packaged for the mainstream non-Muslim customers who seek an ethical low-risk financing – to the virtuous circle Ethical Finance products which would further replace the investment in a base metal by investing solutions closely aligned with the ESG principles – for example, carbon off-sets, sustainable housing, sustainable energy generation etc.

It must be noted that the Sharia-compliant financing tends to be more expensive than the corresponding loans and mortgages offered by the traditional European banks, which is largely due to the higher additional security offered by there being a long-term repayment arrangement ensuring additional security for both the borrower and the lender, as well as the fact that there is less competition in this niche, and comes on top of a typical high own deposit required (at least 20%)4. However, the administration costs are driven by the religious requirements, and as such should be expected to drop if a similar structure were to be used without the religious constraints with the view to the product being sold to the non-Muslim clientele. Additionally, a prospective adoption of the Commodity Murabaha or a similar product by the mainstream banks would undoubtedly drive the costs down by injecting competition into the market.

Our Islamic finance Practice aims to leverage the core principles of Shariah law in transformation projects and are currently gearing up to assist in developing a clear digital transformation vision, navigating regulatory demands and provide end-to-end support to Islamic finance institutions seeking to rapidly integrate innovation and safeguard their infrastructure. With our presence across Islamic countries, we are equipped to support firms with our offerings.

1 CAPCO ISLAMIC FINANCE CAPABILITY APPLICATION OF PEER TO PEER (P2P) LENDING MODEL IN ISLAMIC FINANCE / SHARIAH-COMPLIANT FORM. (n.d.). [online] Available at: https://www.capco.com/-/media/CapcoMedia/Capco-2/PDFs/Islamic-Finance-Campaign_whitepaper_A4_Web.ashx

2 Maidment, P. (n.d.). A Distant Mirror. [online] Forbes. Available at: https://www.forbes.com/2008/04/21/christian-islamic-usury-islamic-finance-islamicfinance08-cx_pm_0421medieval.html?sh=1e5c81a4717b

3 The mortgage time bomb ticking beneath Poland’s banks. (2022). Financial Times. [online] 13 Nov. Available at: https://www.ft.com/content/19235a7a-36f1-41a4-b58f-6adfdea53220

4 Meera, A.K.M. and Larbani, M. (2005). Ownership Effects of Fractional Reserve Banking: An Islamic Perspective. [online] ResearchGate. Available at: https://www.researchgate.net/publication/46545903_Ownership_effects_of_fractional_reserve_banking_An_Islamic_perspective#:~:text=Fractional%20reserve%20banking%20is%20a,basis%20of%20modern%20financial%20architecture.

5 Wait, R. (2022). Sharia Savings And Mortgages Explained. [online] Forbes Advisor UK. Available at: https://www.forbes.com/uk/advisor/mortgages/sharia-mortgages-and-savings-accounts-explained/.