In the light of recent events, U.S. commercial lenders are finding themselves at a pivot point – in search of a new normal. Seismic shifts in the U.S. economy in 2020, driven by COVID and associated business shutdowns, put commercial lenders in a different position in 2021 relative to 2020. A recent research brief from the Richmond Federal Reserve highlighted trends across a wide range of commercial lenders, from regional banks to G-SIBs. When combined with recent trends in lending loss mitigation, this suggests actions which commercial lenders might consider in 2021 and going forward.

Looking at two common segments in commercial lending (C&I, CRE) and a credit segmented impacted by them (securitizations), some key themes emerged in 2020 which impact 2021 :

C&I lending jumped in mid-2020, then trended downward, with a big divergence between small and large U.S. banks. The C&I jump was primarily credit line drawdowns, after which borrowers paid down their lines. PPP lending remained high with little reduction toward year-end. Borrower quality, as measured by internal ratings, trended downward

CRE lending grew slightly in early 2020 but remained flat through year-end. Borrower quality trended downward. Sector performance diverged between warehousing/construction, which remained strong, and hotels/offices/malls, which weakened

For loans held in securitization pools, these credits were subject to similar forces as loans held by originating banks. However, the risk to individual lenders varied based on credit risk mitigation present (loss retention, collateral/guarantees, etc.). When coupled with CARES Act restrictions, the result for CMBS and other structures is a less certain outlook on performance

Across commercial lending in 2020, many banks’ abilities to assess portfolio performance and align strategy with execution was impeded by loan forbearance and forced borrower shutdowns.

Consequently, in 2021, many lenders face net interest margin (NIM) compression and other unanticipated challenges.

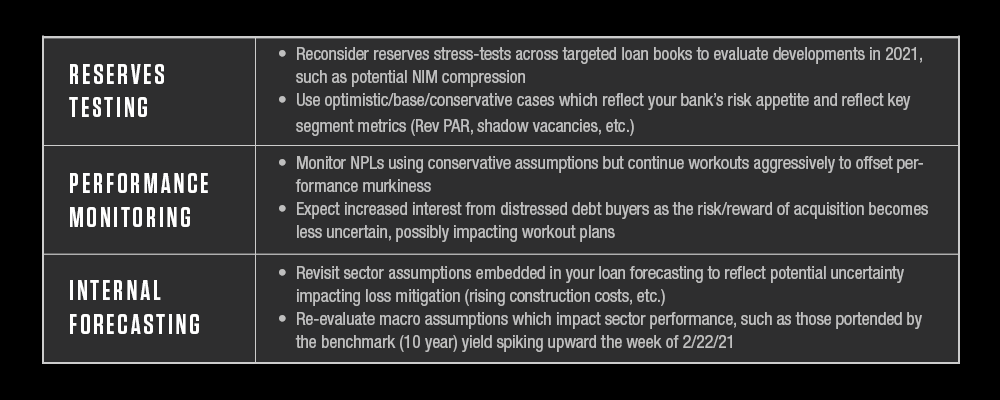

While Q1 2021 continues the trends mentioned above, commercial lenders might anticipate asset and collateral revaluation in Q2 as borrower performance is reported. Based on an executive survey conducted by Capco, implications for commercial lenders include the following:

Portfolio management options, particularly loss mitigation, have taken on new complexity in 2021, give the expected volume later-year defaults across specific segments

While loss reserves per CECL (forward looking) differ from ALLL (historically driven), CECL implementation was pushed out to 2022 for small banks, and large banks have already made big investments in this methodology

In 2Q-3Q 2021, collateral revaluation should be expected that will affect restructuring/bankruptcy options for lenders, which is especially true for distressed CRE

Forbearance broadly impacts mortgage securitization pools, and affects CRE lending for borrowers who were eligible

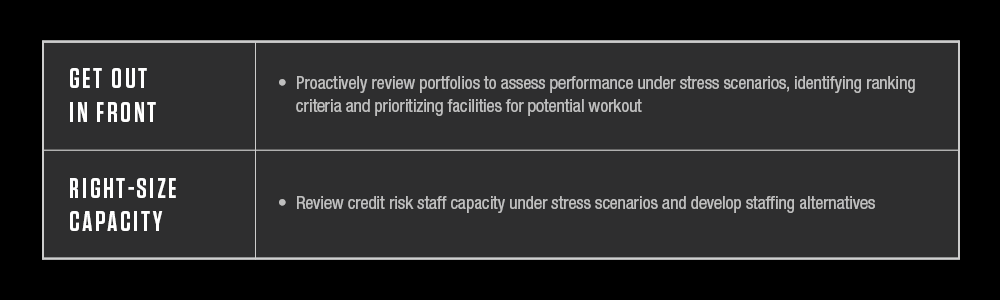

Across the spectrum from G-SIBs to regionals, impact will vary based on individual banks and their business lines. For example, some larger lenders report concerns about risk concentration resulting from embedded terms in their facility and collateral documentation. Others express concerns about conduct risk and associated controls. However, given these common trends, commercial lenders can take specific actions in 2021 to address these concerns.

Commercial lenders can proactively address the challenges presented in 2021 and beyond as market participants recover from 2020. Senior leadership should consider the following:

Capco’s Commercial Banking practice helps commercial lenders, from regionals to G-SIBs, achieve their goals throughout the lending lifecycle. Digital transformation of bank lending has helped firms lower costs and shrink time-to-revenue, but addressing 2021 challenges will involve more fundamental changes, as well. Capco subject matter experts (SMEs) support clients at all phases of their commercial lending journey, from transformation of borrower onboarding to origination, underwriting, portfolio monitoring and performance enhancement. As the market progresses through 2021, Capco can assist banks to do the following:

With these steps in place, Capco can help banks in 2021 adjust to their new normal. To learn more, reach out to the following at Capco: