Consumers’ relationship with their banks is changing across Asia-Pacific as mobile super apps become a principal portal for the purchase of products and services. A notable example of this is the fast-growing Bangkok-based super app Robinhood, which unlike most super apps has a banking industry heritage – it was set up as a subsidiary of SCBX, the holding company of the 116-year old Siam Commercial Bank (SCB).

In this Q&A, Srihanath Lamsam, Robinhood’s CEO, sits down with Chulayuth Lochotinan, Partner and Head of Capco Thailand, to tell him the tale of Robinhood and discuss the lessons learned while building a super app within an established banking group. The two also explore how the super app phenomenon is helping to define the future of banking.

ROBINHOOD’S SUPER APP JOURNEY

Chulayuth Lochotinan: Most super apps grow out of social media platforms or internet services such as ride hailing apps. What led you as a banking group to set up Robinhood?

Srihanath Lamsan: We already had the mobile banking platform, and we’d like customers to make more use of it in their daily life. Once we got into the lockdown resulting from Covid-19, over the last two years, we thought why don’t we try to set up a food delivery platform to help the delivery riders and the restaurants. There were no Thai-owned digital delivery platforms at that time.

So the Robinhood food delivery platform was set up to help small and medium-sized enterprises (SMEs) by charging no commission or GP to the merchant and no commission to the rider – in fact, many of them are tiny businesses, ‘nano-merchants.’ Really we started Robinhood as a Corporate Social Responsibility (CSR) project, and we’ve carried on with much the same philosophy.

Our target is to be the ‘kindest platform’ – helping merchants, riders and consumers by applying something like the ‘paying forward’ concept. It’s unique and different. We are not challenging ourselves to become the No. 1 in food delivery, but instead to become the Alternative Food Delivery Platform.

Srihanath Lamsam, Robinhood’s CEO (left), sits down with Chulayuth Lochotinan, Partner and Head of Capco Thailand (right).

Super apps come in many different forms and are still evolving fast in Asia-Pacific and around the world. In what way is a super app more than just an easy-to-use collection of apps?

Our definition of a super app is that it’s the app you use all the time, right at the top of your applications. So ideally you wake up in the morning and you need to check your balance, maybe order breakfast, buy a ticket for the underground train, and so on – until the consumer uses the super app for 24 hours a day. I think that is the definition of a real super app.

So with super app ownership offering banks a way to deepen and extend the consumer relationship – rather than being pushed into the background as a payments provider – where are you on your journey to becoming a fully-fledged super app?

Today we feel maybe halfway towards it. We’ve built out a series of services to help the customer through their daily life. Next step is to increase the number of subscribers and build out the ecosystem with our partners.

On the Robinhood platform itself, we have 3.2 million subscribers, around 300,000 merchants – 90% of them are really nano-merchants – and about 32,000 riders.

We soft-launched the Robinhood travel business last May – today we can acquire partner hotels nationwide across Thailand, about 15,000 hotels have been onboarded – and we just launched the Robinhood shopping mart. We also hope to have ride hailing early in 2023, allowing our customers to call up a cab or taxi on our platform. So we are lining up our ecosystem.

A bank could become the curator of the 'best of the best' fintech or insurtech, via partnerships, to personalize services to their customers' lifestyles.

There's a common belief that with digital platforms, the winner takes all - the big player takes on the small guy. We think differently - we try to be a friend. It's not a winner takes all concept for us.

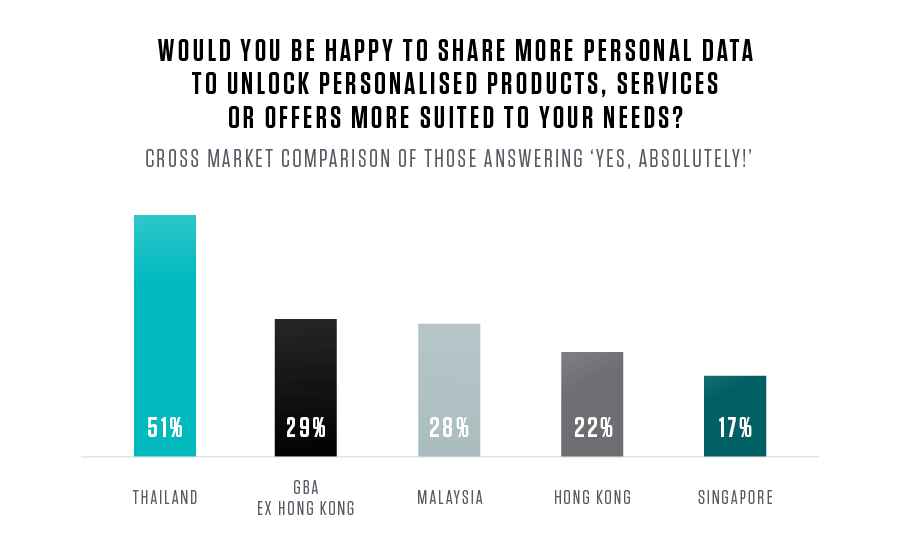

Retail banking services across Asia-Pacific are undergoing seismic transformation, as we recently explored in a survey of the attitudes of 5,000 consumers in five key markets.

ACCESS OUR INSIGHTSWhat does the tale of Robinhood tell us about the bank of the future?

Chulayuth Lochotinan: I think the retail bank of the future is going to be embedded in everyday life, through apps such as Robinhood. Financial needs and transactions are not that interesting to consumers. But you do want to fill your stomach! So the transaction behind that food delivery is still a necessity.

Upfront, though, you will see the things that are immediately relevant to your lifestyle. Meanwhile the bank itself will be seamlessly embedded within these daily-life apps, helping you address your everyday needs. That’s the way to make financial services fun.

Srihanath Lamsam: The bank of the future is going to be an app, and that seems to be true everywhere from the UK and Singapore to Hong Kong and China. And from what we can see, those leveraging different kinds of digital platforms – tech platforms, social platforms, messaging platforms, e-commerce platforms, food delivery platforms – would all love to bring in financial services at a certain point. That’s because one of the biggest portions of the stream of platform monetization is financing, and in today’s economy, investors love to see the P&L!

What could this mean for the shape of the banking industry, and for virtual banks?

Srihanath: In the near future you might see banks unbundle their services, and those who become virtual banks may provide only one service and focus on one target segment such as investment products for the mass consumer.

So in the near future, maybe a virtual bank just provides the deposit for the rider, or only the lending for nano-SMEs. They won’t also lend to big corporations or retail. They are going to focus.

Chulayuth: The bank might well grow into being a specialist by getting really good at one thing, at nano-lending for example. Today there are thousands of fintech and insurtech companies that focus on doing a few things well so, alternatively, once you get a virtual banking licence, a bank could become the curator of the ‘best of the best’ fintech or insurtech. The retail bank becomes a platform that selects the best of the breed, via partnerships, to personalize services to their customers’ lifestyles.

That way, the bank does not have to build everything from scratch anymore, and if the partner is not the best they can switch to another provider of that particular solution. The bank that can do that the best will be a winner in the future.

What is the key to embedding banking into lifestyles – is it the right platform technology?

Chulayuth: Technology is an enabler, but what needs to happen is personalization. The bank needs to know, when you are standing in front of a car showroom, is it because you have already purchased a car and you need car insurance, or because you need a car loan to buy the car? The personalization must be that smart – to offer the right product, at the right time, in line with your personal needs.

Source: Capco, Bank of the Future, 25 November 2022

Or you are driving home one day and an app like Robinhood notifies you that you can order a pizza from your favorite place and have it delivered by the time you arrive back at a click of a button. At the same time, the app should know not to annoy the user with such a notification if the journey is outside their mealtime or they have just been to a restaurant. That kind of super-easy personalization must be completely tailored to the customer’s lifestyle.

To achieve this, you need data and a way to execute your data analytics properly, including an AI engine for personalization. So the technology behind this is very important but it is really an enabler to address the customer and business’s more fundamental needs.

Srihanath: Yes, one of the things I really try to highlight is that the banking service is not actually going to be the one that you try to provide upfront, or that drives engagement. Each financial service is going to be in the background of the platform, so seamless that you don’t really feel that it is a financial service.

However, another key thing for us, is that you have to build up customer engagement not only using technology, but also using the human touch. Not every consumer service can be provided entirely digitally – maybe half of them, but the other half, especially in Thailand, will still use the human touch, to operate the relationship between the platform and the end consumer. It will still be really compelling to have that kind of connectivity and to bond with the customer.