18 October 2022

MAKING DIGITAL GREAT AGAIN: CUSTOMER EXPERIENCE CENTERS

A walk through the changing digital landscape in financial services and how organizations can adopt a dynamic customer experience center.

In the first part of our four-part series, "An Overview of Customer Experience Centers," we explored the return to relationship banking with personalized interactions in customer experience centers (CX centers). In this article, we will dive deeper into consumer behavior and workforce trends that accelerate the need for a digital-first strategy.

Highlights

COVID-19 led to a massive shift in the ways in which customers interact with their financial services providers. Traffic in bank branches has declined significantly, and volumes are not expected to return after the pandemic. Across Canadian bank branches there was a 31% drop in branch traffic from 2019 to 2021, and this trend is likely to persist as mobile app usage increases beyond the pandemic.2 Likewise, in a study by Novantas on U.S. consumer banking, only 40% of respondents said that they expect to return to bank branches post-pandemic.3

While the pandemic accelerated this need for more sophisticated phone and digital banking channels, the trend has existed for nearly half a decade. Between 2016 and 2019, Canadian bank branches decreased by 6%, from 6,190 to 5,820.4 To put it simply, COVID-19 did not kick off the trend, but rather accelerated the change.

In addition to the mass cross-channel migration, customer patience is also waning as companies within other industries (e.g. retail, telecom) modernize their contact centers and streamline customer support within assisted channels. To customers, the nuances of regulatory hurdles within different industries are no longer an excuse for poor customer service, and people are simply asking; “I don’t get put on hold when I reach out to Amazon support, why do I need to wait 30 minutes for my insurance company?”

Highlights

While the concept of a digital bank is not new, the number of digital banks has grown significantly over the past five years, as the Canadian transaction value of neobanks has a 20.42% CAGR, projected to reach US$197.00bn by 2026.5 The rise of challenger banks poses a threat to established retail banks, as consumers across all segments – from baby boomers to Gen Z – are rapidly adopting digital channels as their primary method of banking.6 Due to their digital-first operating models, digital banks, such as EQ Bank, Tangerine, and Simplii Financial, can provide convenient customer service at lower costs, while offering the same security and versatility as their retail counterparts.

Additionally, in recent years, the proliferation of open banking7 and screen scraping8 has created a more competitive financial services landscape, due to an influx of smaller and nimbler fintechs that build competing investment and financial management services on the backs of retail banking data. Recent research showed that Europe had approximately 12 million open banking users in 2020 and it is estimated that it will reach 64 million by 2024.9 Open banking and screen scraping technologies have acted as a catalyst for greater competition, as customer data is no longer the exclusive property of financial institutions, but rather any fintech with which customers agree to share data. Not only are these emerging fintechs smaller and nimbler, but they are also more digitally advanced than traditional banks. This allows emerging fintechs to quickly adapt to changing market demands while building more digitally engaging user interface experiences for banking customers.

The increasing competition from digital banks and other fintechs will continue challenging retail banks to deliver more comprehensive and convenient customer service through digital channels, while offering seamless omnichannel experiences that differentiate them from emerging challengers.

Highlights

Millennials are emerging as the largest demographic of consumers with disposable income, which underscores the need for banks to prioritize digital maturity: 49% of millennials ages 18-3410 switched or considered switching banks in the last 12 months to receive a better digital experience. This compares to an average of 27% across all age groups, indicating that millennials place a greater value on digital banking and customer service than the general population. In addition, according to a study by FICO, negative customer experience is one of the top reasons why millennial customers switch banks.11 This frustration with the lack of digital maturity in customer service will only continue to grow, as over half of millennials find difficulties in resolving problems with their bank as a sufficient reason to leave.12

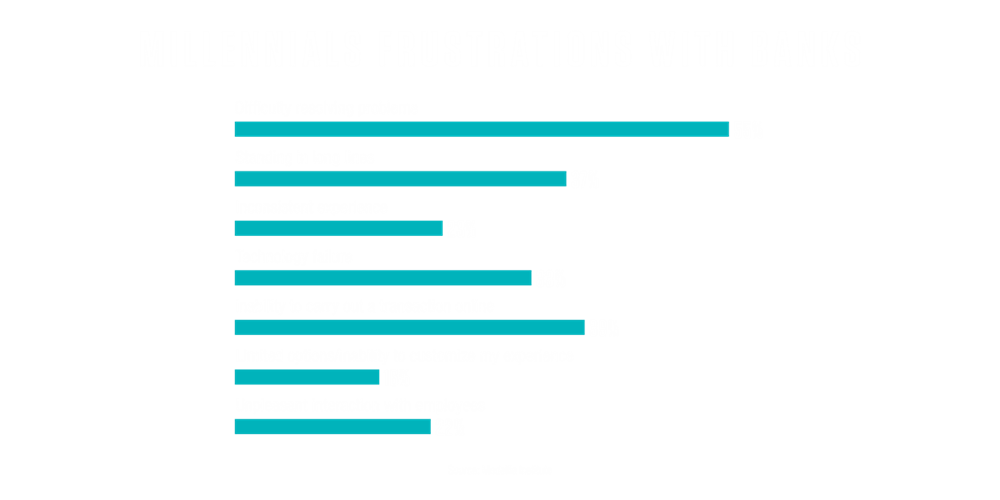

While the desire for ‘better digital experiences’ is broad and abstract, a study by the UK Current Account Switching Service (CASS) reveals in more detail the breakdown of top non-financial reasons for switching banks13:

The top non-financial drivers of customer attrition are related to digital experiences and customer service, where traditional retail banks often lag their digital bank counterparts. Therefore, established banks should prioritize CX centers now more than ever to retain millennial customers and attract emerging Gen Z customers.

Highlights

Competition is high not only for customers but also for talent. The International Customer Management Institute14 pegs the average contact center turnover rate at 33%, and the average cost of replacing a contact center agent is roughly $10,000.15 This means that for large retail banks where contact center employees number in the tens of thousands, the cost of attrition can exceed $100M a year.

With shifting ways of working, this issue will be increasingly problematic if organizations don’t act now to improve employee experience and engagement. Contact centers primarily compete for agents in the local area of their physical offices, which limits the supply of labour, but also limits the competition for talent from other contact centers. However, due to the global shift towards work-from-home as the new normal – and contact center as a platform (CCaaP) technology that enables remote agents – competition for talent has drastically increased.

Aside from salary, some of the top reasons for agent resignations at contact centers include:

High attrition within contact centers not only affects operational costs but also weighs down customer satisfaction due to unmotivated and poorly trained agents. To reduce this attrition, organizations must offer fewer menial tasks and more complex work that can lead to meaningful career advancement. In addition, organizations are responsible to supply their agents with the necessary tools to support customers seamlessly and logically.

As consumers increasingly want convenient and thoughtful banking experiences and contact center agents seek more career development pathways, customer experience centers provide the key to unlocking customer acquisition and employee retention.

In the third part of the four-part series, Traditional Contact Centers vs. Customer Experience Centers, we will explore how a customer experience center provides these benefits in contrast to traditional contact centers.

_____________________________________________

1 https://cba.ca/bank-branches-in-canada

3 https://www.novantas.com/industry-insight/novantas-review/2020-summer-analyzing-customer-traffic/

4 https://cba.ca/bank-branches-in-canada

5 https://www.statista.com/outlook/dmo/fintech/neobanking/canada

6 78% of Canadians use digital channels to conduct most of their transactions. Canadian Bankers Association https://cba.ca/surging-use-of-digital-banking-accelerates-during-the-pandemic-cba-survey

7 Open banking involves the use of open Application Programming Interfaces (APIs) that allow 3rd party developers to build applications and services by interfacing with the databases and services of larger financial institutions

8 Screen scraping is the act of copying data from one source into another. It is often used as a temporary solution for transferring banking data in countries that have not yet adopted open banking. This method is much less secure than open banking, as the destination application requires the user to provide login information to their bank

10 https://www.mulesoft.com/press-center/trends/2019-consumer-research-financial-services

11 https://www.fico.com/en/newsroom/fico-survey-millennials-2-3-times-more-likely-switch-banks

14 https://www.icmi.com/resources/2016/reducing-attrition-in-contact-centers

15 https://swpp.org/winter-2017-ontarget/true-cost-of-attrition/