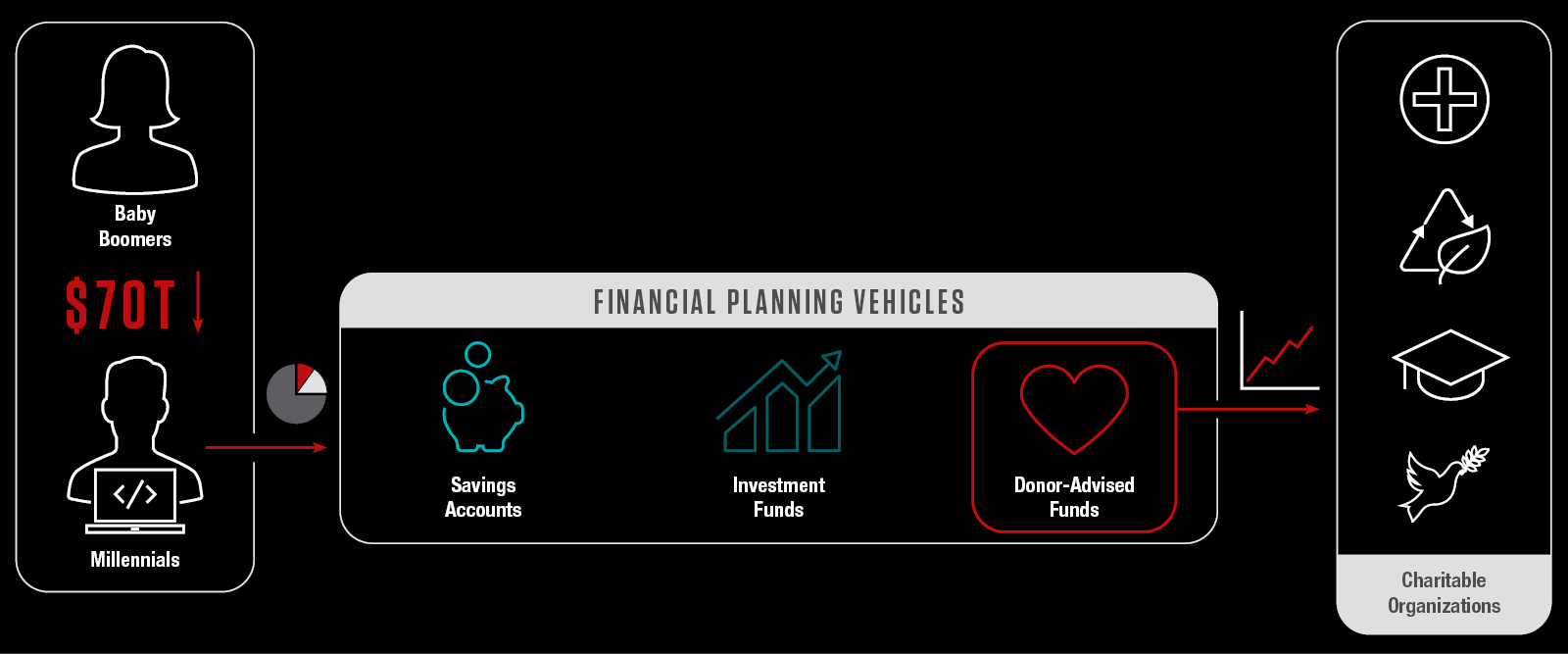

An impending $70 trillion generational transfer of wealth, coupled with shifting financial priorities among the recipient demographic, makes for a ripe opportunity for financial services firms to capture market share and expand their competitive advantage. The question now becomes: how?

Within the next 20 years, it is expected that the Baby Boomer generation will have transferred $70 trillion in wealth to their Millennial heirs. As of today, the Millennial generation makes up America’s largest age demographic, home to 95 million 25-to-40-year-old members whose cultural preferences, and outlooks, are already significantly shifting today’s financial markets. This generation is more health conscious, technologically savvy, educated, and most importantly – considered to be more philanthropic than their Baby Boomer predecessors, as evidenced by a recent Fidelity Charitable report which indicates Millennials give more than twice as much money and time to charitable causes then those of the Baby Boomers or Gen X demographics.

Historically, investment vehicles for charitable giving were only available to HNW and UHNW given the benefits regarding tax optimization, but for mass affluent customers, this was rarely considered a top priority. Given this shifting landscape, a significant opportunity presents itself as an advantage to financial institutions looking to cater directly to this mass affluent Millennial market: Donor-Advised Funds. DAFs are an investment product which, unlike traditional donor options, are not exclusively reserved for high-net-worth customers, which enable individuals to contribute to charitable organizations in a meaningful manner. The use of such investments results in substantial tax benefits and can be structured in various manners. As such, with enhanced platform development enabling the democratization of philanthropy, allowing the average investor to centralize individual contributions, it is critical that DAFs are placed at the forefront of a financial institution’s product offerings to capture incoming assets being handed down to the ever-changing landscape of investors.

In short, DAFs are a philanthropic financial product which can be described as a charitable investment account designed for individuals to support IRS-approved charitable organizations. When such individuals contribute to a DAF, they become eligible to take an immediate tax deduction. Subsequently, these funds can be invested to grow tax-free, and donors can recommend grants to a variety of qualified charities. Individuals can make tax-deductible donations via a wide array of assets including cash, stocks, or non-publicly traded assets, such as private business interest or cryptocurrency. Typically, sponsoring organizations have a variety of investment options which individuals can leverage as part of their customized investment strategy.

Aside from the immediate tax deduction, there are several benefits correlated to the utilization of DAFs which can be realized by investors, including but not limited to:

While the benefits of DAFs are versatile and extensive, they are not exclusively limited to the charity or investor. As previously mentioned, there is a massive upcoming transfer of wealth projected and therefore, financial institutions which offer DAFs will have a significant market advantage in managing this wealth by directly catering to this more philanthropic demographic. This will not only lead to increased client loyalty but will also result in reaching a larger target market, ultimately yielding enhanced AUM levels for these institutions. While industry leading institutions, such as JP Morgan and Merrill Lynch, already have frameworks in place to accommodate such investment opportunities, this has rarely been reported as a priority for their mass affluent customers. Often being attributed to not having enough awareness on tax-optimizing benefits, competing firms can gain a market advantage by targeting this niche market.

“The future of charitable giving is undoubtedly digital, and with solutions, like Louise, advisors can offer clients a world-class giving experience today. Offering tech-enabled, personalized DAFs fosters can involve the entire family in giving and marks a new era of more impactful philanthropy,” says Cor Hoekstra, GM of Louise by TIFIN.

Louise by TIFIN, a digital charitable giving platform, is a fintech company that empowers financial advisors to grow their practices by introducing DAFs into the client experience, allowing for more efficient and effective utilization. Not only can financial services firms optimize their product offering by leveraging platforms, such as Louise, but they can further expand their customer base as many platforms democratize contributions, expanding such offerings to investors who previously did not have the capital to do so.

“Over 1 million donors already use DAFs as their giving vehicle, made easier by the adoption of technology. Digital DAFs bring lower fees with no account minimums, empowering donors across a range of ages and financial means to make an impact on the causes they care about most, while maximizing tax efficiencies,” Cor continues.

Such frameworks significantly alter the pre-existing notion that philanthropic financial products are reserved exclusively for ultra-high-net individuals, allowing firms to enhance their overall branding efforts and simultaneously cater to this Millennial market. With this in mind, it is evident that DAFs are a critical component within the wealth space, and now is the time to take advantage of such offerings.