18 October 2022

MAKING DIGITAL GREAT AGAIN: CUSTOMER EXPERIENCE CENTERS

A walk through the changing digital landscape in financial services and how organizations can adopt a dynamic customer experience center.

For centuries, since the creation of the first bank, relationship banking has been the key strategy in customer retention. It provides customers with a single point of service where the financial institution understands the customer at a deeply personal level and tailors their products and services towards the true financial needs of the customer.

With the rapid advancement of technology over the past two decades, there has been immense pressure on financial institutions to cut costs, streamline customer interactions, and diversify their customer base. In addition, the barriers for switching banks are being torn down, and the reasons for switching are increasing as more players enter the market and the competition becomes fiercer. Combined, these trends have driven financial institutions from the traditional relationship banking model towards a more transactional banking model, where the quantity of interactions resolved and reduction in cost per interaction are prioritized over the quality of each customer relationship.

While the diversion of focus towards transactional banking has served banks well (with significant cost efficiencies in customer service and record-breaking profit growth), the lack of focus on relationship banking is slowly eroding customer satisfaction in the largest financial institutions. This is reflected in a survey conducted by J.D. Power, which found that overall satisfaction in the big 5 Canadian banks declined by three points between 2020 and 2021, while satisfaction in mid-sized banks (which tend to be more digitally mature) improved by 12 points in the same timeframe.1

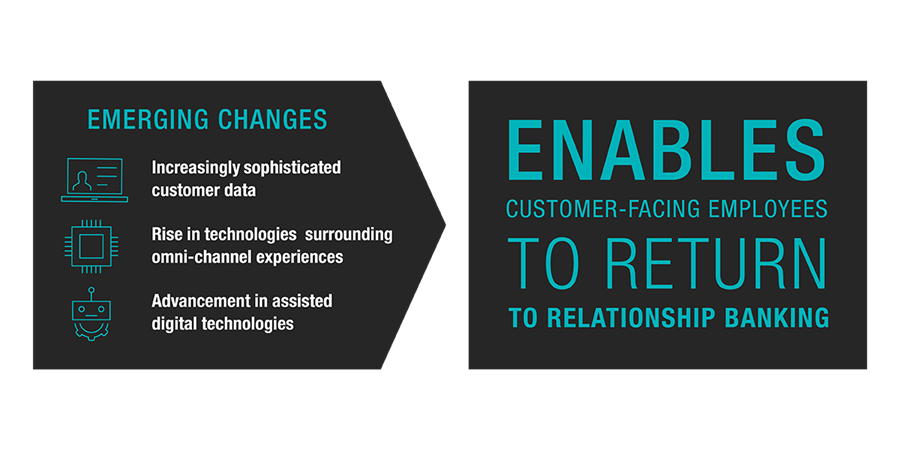

To harness the potential of these emerging technologies, organizations must stop viewing their customer interaction channels as isolated pathways to service customers – and start thinking about the customer experience across all channels. To enable this transition, organizations must move away from the contact center support model to a CX center model.

The difference between a contact centre and a CX centre lies in the concept of a cross-channel ecosystem, which brings together human and technological functions to improve the customer journey and motivate employees.

It allows customers to engage with organizations in the most accessible and convenient way by allowing for:

1. Seamless transition between channels – Applying the right processes and technologies to ensure customers can jump between self-serve, assisted, and in-person channels seamlessly without any loss of information

2. Leveraging predictive analytics to anticipate customer needs – Shifting from a reactive to a proactive approach in sales as well and servicing, so customer needs get addressed before they need to reach out

3. Tying customer experience directly to employee experience – Enabling employees with more autonomy and meaningful work so they feel empowered to address customer needs rather than complete menial tasks

4. Incorporating self-serve and employee assisted capabilities – Leverage data and technology to redirect customers to the right channels (assisted or self-serve) for their needs, ensuring the purpose of each channel is fully utilized

Simply put, CX centers lay the groundwork for making digital great again after an era of transactional banking.

The idea of bringing these pillars together to improve customer experience may seem intangible, we will explore in further details on CX Centre in the series.

In the next instalment of this 4-part series, we will discuss the current market trends affecting the need for greater adoption of assisted digital experiences and what makes customer experience centers more important now than ever before.