In the first of this three-part series, we identify six fundamental technology trends set to transform commercial insurance. We then explore how core technology architectures are evolving differently in each of the SME, mid-market and large corporate segments. The next two articles in the series take a similar approach to explore the transformation of underwriting and broker connectivity.

Speed read

- Commercial insurers need to act on key technology drivers such as cloud-enabled core modernization, modular architectures, standards-based connectivity, and Agentic and GenAI.

- Transformation in each market segment will be shaped by different imperatives, e.g. SME by scalability and mid-market by segment convergence.

- C-suite executives need to develop segment-specific transformation strategies while also engineering shared foundations across the business.

- The choice between ‘centralized’ versus ‘federal’ versus ‘hybrid’ should be made at the executive level. Meanwhile, GenAI will not deliver sustained ROI without curated data, strong controls and integration into workflows.

In a market defined by macroeconomic volatility, competitive saturation, and shifting customer expectations, commercial insurers face a new strategic imperative: performance is no longer determined primarily by where they play, but by how effectively they adapt their operations to an evolving market.

This means understanding what is driving change and what is required in terms of the ability to execute transformations.

Technology trends driving change

Capco’s five-year vision of the transformation of commercial insurance is organized around a set of reinforcing trends, already visible in the market and now accelerating:

- Cloud-enabled core modernization becomes unavoidable. Capco’s outlook highlights an industry push to modernize legacy platforms with scalable, cloud-based solutions to enable operational efficiency, real-time processing, and straight-through processing (STP). Legacy policy administration systems will be modernized or augmented to enable STP of routine transactions, real-time data exchange and advanced analytics.

- Modularization becomes the default architecture pattern. Insurers will increasingly adopt microservices and event-driven architectures that support easy integration of new capabilities, such as IoT data feeds and external risk models, without overhauling entire systems. The focus will be on selective core upgrades – replacing parts of the engine rather than the entire system – to incrementally add agility and analytics. This will help commercial insurers avoid the cost and risk of ‘big bang’ replacements.

- End-to-end digitization across the value chain shifts. Capco’s view is that competitive advantage increasingly depends on digitizing the entire broker–insurer–reinsurer chain, much of which remains manual today. The next five years will see commercial insurers moving from aspiration to infrastructure implementation. Agentic AI and intelligent workflows will automate repetitive tasks in underwriting support, e.g. data entry and clearance checks, and in back-office processing.

In personal lines the transformation has already begun, e.g. in recent years, Allianz Partners has begun enhancing and replacing earlier RPA bots with more advanced AI systems to process simple travel insurance claims.1 In commercial underwriting, automation will tackle submission intake and triage – as we discuss in the second article in this series – as well as policy issuance including auto-filling data once terms are agreed. It will also facilitate compliance checks, e.g. by automatically flagging sanctions or regulatory issues. The goal is a ‘digital assembly line’ from submission to policy bind, where human intervention is only required for complex exceptions. Fully digital workflows across brokers and Managing General Agents (MGAs), carriers, and reinsurers will unlock benefits that include streamlined operations, fewer errors from rekeying data, and faster decision-making across the industry.

- API ecosystems and standards-based connectivity become the operating model for distribution and trading. ACORD’s ADEPT is a particularly interesting recent development that positions itself as a one-to-many placing interface and ‘single letterbox’ for insurers. It allows them to exchange standardized placing data with brokers and multiple placing platforms so firms do not need separate integrations with each one. This is not just a London-market story: ADEPT hubs are expanding geographically, underscoring the market ambition to industrialize structured data exchange at scale.

- AI and GenAI will be embedded in insurance processes. Artificial intelligence will be deeply embedded in underwriting and operations. Machine learning models will support underwriting by analyzing historical loss data, predicting risk trends, and even recommending coverage terms or pricing adjustments.

Generative AI (GenAI), in particular, will play a transformative role in handling unstructured data and knowledge tasks. Large language models can automatically read and summarize submissions, highlight key exposures in lengthy reports, and even draft policy wording suggestions. This knowledge augmentation will streamline underwriters’ work, e.g. AI can pull relevant clauses or past claims from databases in seconds, whereas a human might spend hours searching.

- GenAI will accelerate core modernization. The role of GenAI is not just as part of the end-state architecture, but as a delivery catalyst throughout the transformation lifecycle. In insurance, where legacy systems and long project timelines are common, GenAI offers tangible acceleration. In early stages of the Software Development Life Cycle (SDLC), GenAI can translate business requirements into user stories in Jira, streamlining the design phase.

For policy migration, it can suggest mappings and extract logic from legacy documents, speeding up conversion and validation. When modernizing COBOL-based Policy Administration Systems (PAS), GenAI helps refactor and translate business logic into modern code. Finally, during testing, it can generate test cases and synthetic data.

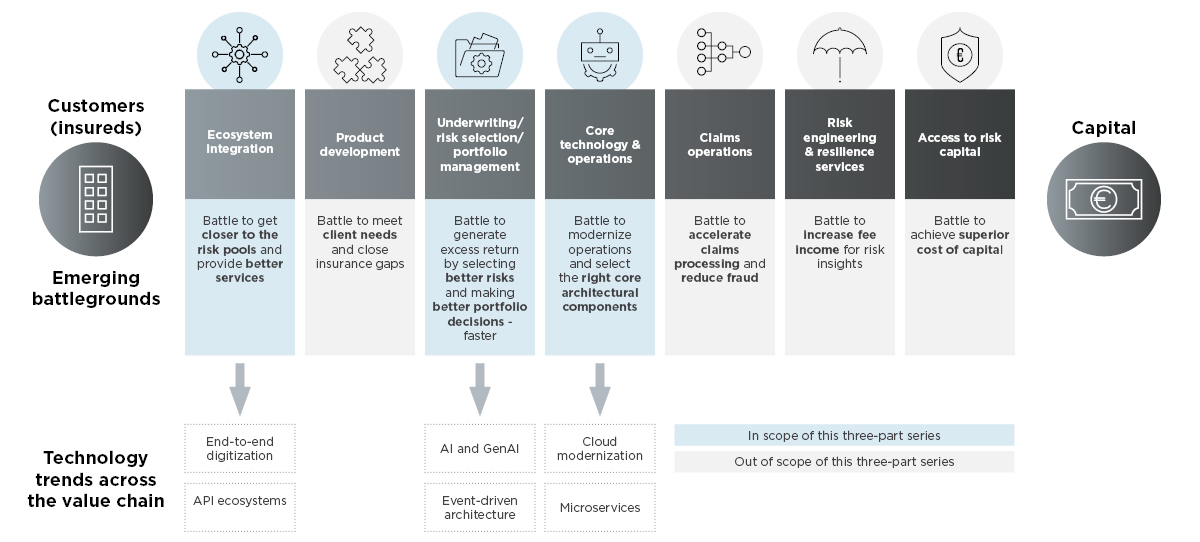

These trends are fueling a series of tech-driven competitive battlegrounds across the commercial insurance value chain, as our Figure below sets out. The technology trends are closely interrelated and have a clear implication for senior executives. The next five years are less about ‘buying tools’ and more about recasting commercial insurance as a digitally connected, data-driven operating system, tailored by segment.

Tech-enabled battlegrounds across the value chain

Core technology evolution by segment

Next we explore what this means for modernizing core architectural components such as Policy Administration Systems (PAS). As each segment requires different operating models, we will look in turn at SME, mid-market and large corporate insurance businesses.

SME

In the SME segment, insurer architecture is dominated by volume economics and speed: platforms must support high-throughput quoting, servicing, and claims with low unit cost.

The five-year architectural shift is toward a cloud-enabled core where product and pricing changes are configuration-led, not code-led. This will be essential so that carriers can keep pace with distribution demands and competitive pricing, while still maintaining control.

‘Digital servicing at scale’ will become a competitive advantage and will offer features such as automated cancellations, mid-term adjustments, renewals and certificate generation. These in turn will trigger consistent downstream updates – documents, billing, accounting entries – via event-driven integration.

Mid-market

Mid-market architecture must balance moderate volume and moderate complexity, with many insurers now re-thinking their architectures. Some have extended their high-volume SME platforms upwards, e.g. by adding more flexible rating rules or underwriter referral workflows to handle slightly more complex mid-market submissions.

Others have scaled down their large account systems, creating templates for mid-market package policies to speed up processing. Notably, leading carriers are pursuing segmented platform strategies. For example, in 2025 Chubb merged its lower middle-market and digital small business units into a single division to build a unified, scalable platform for small-to-mid commercial customers.2 This reflects an architectural trend to leverage common systems for SME and the lower end of mid-market to maximize efficiency.

Large corporate

Large corporate architecture is a different problem: it is defined by complexity, multi-line programs, cross-border issuance, and heavy regulatory and tax variation.

The technology architecture for large corporate insurance has historically been the most legacy-laden and siloed, but this is now changing as leading insurers invest in modernization. Large commercial carriers often operate multiple complex policy administration systems – sometimes one per major line or region – to handle bespoke policy terms, large schedules of assets, global program issuance, and compliance across jurisdictions.

These core systems prioritize flexibility and robustness over volume scalability, because they must handle very large policies with custom terms and significant data ingestion, e.g. thousands of fleet vehicles or property locations, and intricate pricing models. Many large-risk platforms take the form of older mainframe or heavily customized solutions, reflecting the bespoke nature of the business. However, top-tier insurers are now transforming these architectures to become more agile, connected and centralized.

The natural shift in the coming years will be to move toward a global hub-and-spoke model. That is, a (near) central master platform for multinational programs, integrated with local issuing entities/partners for admitted policies and claims handling – all supported by orchestration, common data models and strong governance.

Core architecture trends by segment – summary

From vision to execution

Our discussion supports several key takeaways for senior executives. The first is that C-suite executives at leading commercial insurers should adopt segment-specific transformation strategies, while also engineering shared foundations across the business.

This is because the technology architectures required in the SME, mid-market, and large corporate segments will remain significantly different. However, leading insurers will increasingly share foundational capabilities across segments in areas such as cloud-enabled core services, common data products, orchestration, and identity/security patterns. They will then need to use these foundational capabilities to adapt the workflow and customer experience layer to suit each segment.

Leaders should modernize their technology with discipline: the choice between ‘centralized’ versus ‘federal’ versus ‘hybrid’ is not a technical detail and should be made at the executive level. The strategic question for leadership is: where must you standardize to scale, and where must you localize to win? Our view is that while the core should be kept as central as possible, the platforms facilitating the placement of the risks should be adapted to local market conditions.

As our discussion of the key technology trends makes clear, commercial insurers must make data orchestration and AI governance ‘day one’ foundations. GenAI will not deliver sustained ROI without curated data, strong controls and integration into workflows. Furthermore, governance must be designed in from the start to meet regulatory expectations, e.g. around explainability and human oversight. Gen AI, however, can also be used improve development, testing and transformation program velocity in core technologies and elsewhere.

The technology trends that we have identified mean that commercial insurance must be reengineered over the next five years as a digitally connected, data-driven operating system, tailored by segment. The right vision will not be enough: transformation programs will need to be governed with realism, aligned to operating realities, and designed for phased delivery.

The right executional mix will be needed to sustain transformation over the next five years, leveraging partners that can execute end-to-end, not just advise. Capco’s strength lies in combining core modernization, underwriting redesign, GenAI implementation and large-scale integration with deep domain expertise in insurer governance and change management.

Read the second article in this series to explore how commercial insurer underwriting is about to be transformed.

References

1 https://www.allianzworldwidepartners.com/usa/media-center/press-releases/Allianz-Partners-launches-new-claims-portal-and-adopts-AI-to-take-customers-experience-to-the-next-level.html

2 https://news.chubb.com/2025-03-12-Chubb-Creates-New-North-America-Small-Lower-Midmarket-Division