In the first two parts of this series, we explored how key technology trends will shape core technology and underwriting processes in commercial insurance. Here we move on to explore how technology will also transform distribution and broker connectivity in different ways across SME, mid-market and large corporate segments. We conclude by bringing together seven key executive takeaways that span our series to point the way toward successful commercial insurer transformations.

Speed read

- Broker and Managing General Agent (MGA) integration and digitization is a key lever in commercial insurance transformation, but varies significantly by sector.

- Success in the SME segment depends on full integration into e-trading ecosystems; in mid-market, triage, speed and tailored solutions for engaged brokers are key; for large corporates, commercial insurers must support the broker relationship by reducing frictions.

- Executive takeaways include treating broker integration as a growth leader. At the series level, key takeaways include adopting segment-specific transformation strategies with shared foundations, and prioritizing data orchestration and AI governance as foundational.

- Over the next five years, commercial insurers will win by modernizing the core and data foundation, industrializing bionic underwriting, and integrating into broker-led placement ecosystems.

Broker and MGA integration is becoming one of the most decisive levers in commercial insurance transformation. It has a direct and increasing impact on the quality of the information submitted by the broker to the MGA, quote speed, operating efficiency, and broker loyalty.

Yet how insurers engage with broker and MGA partners varies significantly by segment. At the SME end, success depends on full integration into e-trading ecosystems. In mid-market, speed and tailored solutions for engaged brokers are key. In the large corporate segment, the shift is subtler and means supporting the broker relationship through data-sharing, workflow orchestration and reduced friction.

At the heart of this shift is the increasing digitization of risk placement platforms and market-wide digital initiatives such as Lloyd’s Blueprint Two (although that ambitious program is paused for now). These ecosystems standardize and streamline how brokers and carriers interact:

- Input – A broker enters client data into a broker portal or Agency Management System (AMS).

- Standardization – Data is structured using ACORD standards, the global data and messaging standards for the insurance industry, creating a common language across platforms.

- Transfer – APIs transmit that data through gateways (like ADEPT) to a placement hub.

- Placement – Insurers receive submissions, negotiate digitally, and bind risks via shared platforms.

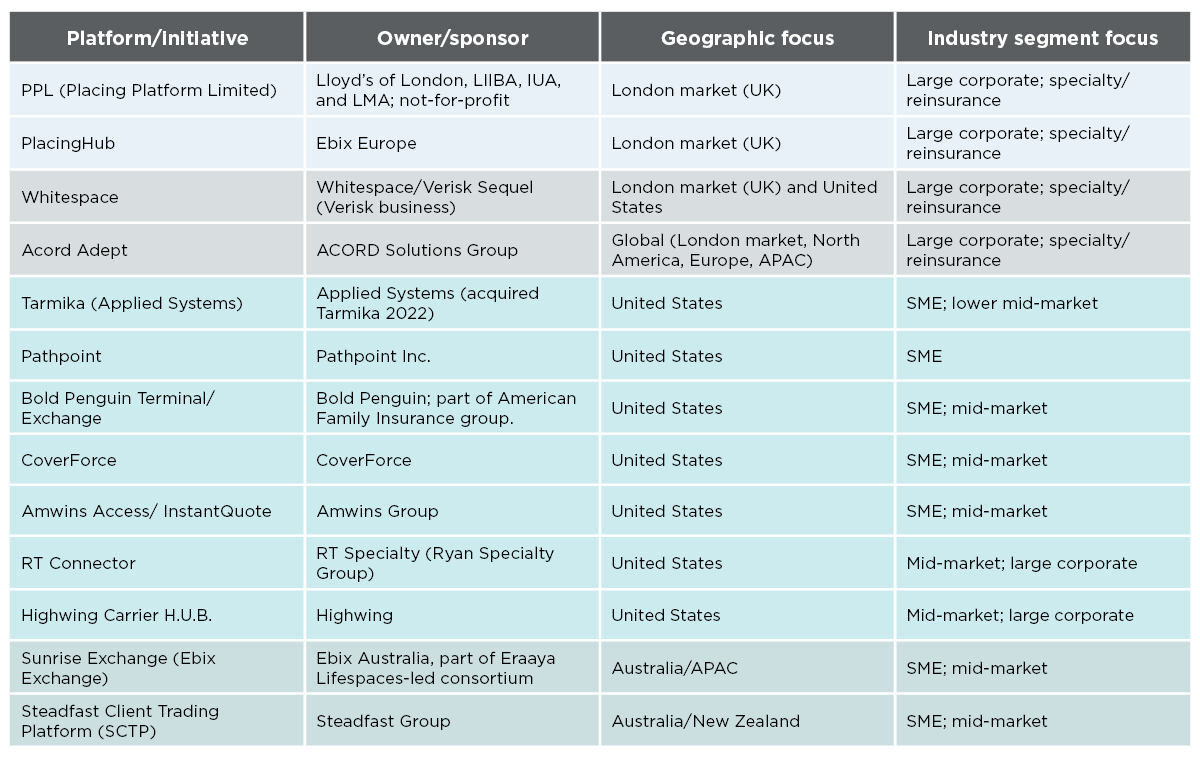

These shared platforms – such as PPL, Whitespace, Sunrise – represent the new infrastructure for commercial distribution, although the platforms vary in terms of their origins and ambitions. In the table, we summarize the key platforms and initiatives, their owners and sponsors, and their geographic and segment focus.

Market integration - key platforms and initiatives

In the following sections, we compare broker and MGA integration across the SME, mid-market, and large corporate segments, examining submission methods, platform usage and levels of digital maturity.

SME

The SME segment has seen the most advanced digital integration with brokers and other channels. Here, platform-based distribution is the norm in many markets. Insurers distribute small commercial policies through a variety of interconnected channels: broker portals, price comparison websites, agency management system integrations, and even direct-to-customer online platforms for very small businesses.

Broker portals provided by insurers allow brokers or agents to quote and bind policies 24/7 with minimal insurer intervention. In some markets, e.g. the UK, brokers use e-trading platforms that aggregate quotes from multiple insurers for standard SME risks. Insurers must integrate into these platforms or risk missing out on business.

API connectivity is crucial: insurers need to integrate with external APIs, adopt market standards, and digitally support third-party providers to activate broker and aggregator channels. This means a broker’s software can ping an insurer’s system in real time for a quote, and the insurer’s answer comes back instantly, fitting into the broker’s workflow. Many insurers also support upload of standardized data schemas, such as ACORD XML, so that brokers can submit information from their systems without re-keying.

Delegated authority arrangements are also widespread in the SME arena: insurers often empower MGAs or large brokerages with binding authority for certain small business products. Under these delegated underwriting schemes, the intermediary uses the insurer’s guidelines and systems to underwrite on the insurer’s behalf.

Submission methods in the SME segment will evolve towards being entirely digital, with small business submissions typically involving filling out an online form or transmitting data electronically. Email or paper submissions will become the exception. Digital maturity in this segment, already high, will continue to evolve as the process from application to policy issuance is fully automated for many products.

In addition, many SME customers (especially younger entrepreneurs) expect a seamless digital buying experience like that in personal lines – pushing insurers and brokers to innovate. Some insurers offer self-service portals where business owners can get quotes for and purchase simple coverages (e.g. general liability or a business owner’s policy) in minutes. Players increasingly compete on who can deliver quotes fastest and integrate with the most channels.

Mid-market

The mid-market segment has historically been underserved in terms of dedicated models, often falling between the cracks of big broker focus and small business automation. However, broker integration in mid-market is evolving quickly as this segment gains strategic attention.

Mid-market clients often still use brokers (sometimes regional or specialized brokers) to advise them, but these brokers may not have the same resources as the global firms. Insurers are therefore finding ways to streamline submissions and quotes for mid-market brokers to win business.

Many insurers provide broker portals or extranets for mid-market submissions: a broker can log in, input a client’s basic information and coverage needs, and receive either an instant quote for simpler cases or confirmation that an underwriter will review. Email submission is still common for complex packages, but leading carriers are starting to digitize the intake by encouraging brokers to use structured online forms or upload data through web interfaces.

API integration is less mature than in the SME segment but will grow, e.g. insurers might integrate with broker management systems (like Acturis or Applied) to fetch submission data directly. The types of platforms used can include multi-insurer portals that cater to mid-market risks in certain markets, although if a risk is highly bespoke it goes outside those platforms.

Delegated authority in mid-market exists in select areas, such as niche programs where an MGA underwrites mid-sized accounts on behalf of insurers. More generally, mid-market risks are often individually underwritten by carriers.

The digital maturity of mid-market distribution is moderate and uneven, but this is about to change. Crucially, the industry has recognized that mid-market requires its own approach: these clients often lack internal risk managers and can feel ‘deprioritized’ when neither the high-end brokerage model nor the automated small business model serves them well.

To address this, insurers are strengthening broker partnerships and specialization for mid-market. We also see carriers and brokers collaborating on industry-specific platforms or facilities to handle mid-market business more efficiently. The emerging model is more consultative (brokers as advisors) and more digitally supported (for speed and efficiency).

Carriers that get the formula right stand to gain significant market share. With an estimated $150+ billion addressable premium in the mid-market, and no carrier having more than 5% share, this segment represents a huge opportunity if it can be served properly.1

Large corporate

The large corporate segment is dominated by global brokers and bespoke brokerage engagements. These clients typically have dedicated internal risk managers and use major brokerage firms (Marsh, Aon, Willis, etc.) to negotiate coverage.

Integration with brokers here is mostly high-touch and relationship-driven, rather than via standardized digital portals. Submissions for large accounts often arrive as extensive proposal documents, spreadsheets of exposures, and engineering reports sent via email or data rooms.

There is little use of generic quote portals. Instead, brokers and underwriters negotiate terms through meetings, calls and correspondence. That said, insurers are beginning to adopt tools to streamline the exchange of information: for example, some participate in electronic placing platforms (like Lloyd’s PPL or similar systems) for certain lines, and others are building APIs to ingest broker data directly into underwriting systems.

Overall, though, digital maturity is lowest in this segment’s distribution. The process is bespoke: brokers craft tailored submissions and underwriters craft tailored solutions. The broker platforms used are often the brokers’ own systems – large brokers might have internal systems to manage large account placements, and insurers may need to integrate with those on a case-by-case basis.

For instance, a large broker might electronically send a market submission to an insurer’s intake system if both have agreed on a data exchange format; otherwise, it is handled manually. Delegated authority is rarely used for true large corporate risks, since insurers prefer direct oversight on these high-value, unique accounts – with a few exceptions in specialty markets or fronting arrangements.

In summary, broker integration for large corporate insurance will remain characterized by personalized interaction and bespoke negotiation, with technology playing a supporting role (e.g. tracking submissions, sharing data) but not providing a fully automated interface. We may see more data-sharing APIs to streamline complex placements, but technology will largely make administration and information exchange more efficient rather than replace broker collaboration.

Broker/MGA integration trends by segment – summary

Executive-level transformation takeaways

In this concluding section, we bring together the key takeaways spanning our series. Across the transformation of core technologies, underwriting processes and ecosystem integration the most common executive mistake is to treat transformation as a linear IT program. Success instead depends on aligning technology modernization, analytics, and operating model change across the value chain.

The following seven imperatives are therefore critical to commercial insurer C-suites, regardless of where the carrier competes:

- Adopt a segment-specific transformation strategy but engineer shared foundations. The technology architectures required by commercial insurers in the SME, mid-market, and large corporate segments will remain significantly different. However, leading insurers will increasingly share foundational capabilities in areas such as cloud-enabled core services, common data products, orchestration and identity/security patterns. They will then adapt the workflow and customer experience layer to suit each segment.

- Modernize the core with discipline: centralized vs federal vs hybrid is an executive choice, not a technical detail. The strategic question for leadership is: where must you standardize to scale, and where must you localize to win?

- Make data orchestration and AI governance ‘day one’ foundations. GenAI will not deliver sustained ROI without curated data, strong controls, and integration into workflows. EIOPA’s explicit expectations around explainability and human oversight mean governance must be designed in from the start.

- Industrialize bionic underwriting to increase capacity and improve decision quality. Executives should first target a reduction in the amount of time that underwriters spend on administration, and then expand into analytics-driven insights and GenAI document intelligence.

- Treat broker integration as a growth lever. With the rise of platforms like Whitespace and Acord Adept, KPIs like speed-to-quote and post-bind query volumes now directly influence broker preference and growth.

- Accelerate transformation with GenAI and disciplined delivery. Gen AI can improve development, testing and program velocity, so long as governance and architectural convergence are maintained.

- Choose partners that can execute end-to-end, not just advise. Partners must combine key strengths such as underwriting redesign, GenAI implementation, large-scale integration, governance and change management if transformation is to be coherent and sustained over the next five years.

Taken together, the executive message is straightforward: over the next five years, commercial insurers will win by modernizing the core and data foundation, industrializing bionic underwriting, and integrating into broker-led placement ecosystems – while governing AI responsibly and executing transformation with disciplined delivery.

The right executional mix will be needed to sustain transformation over the next five years, leveraging partners that can execute end-to-end, not just advise. Capco’s strength lies in combining core modernization, underwriting redesign, GenAI implementation and large-scale integration with deep domain expertise in insurer distribution, governance and change management.

References

1 https://www.insurancebusinessmag.com/uk/news/breaking-news/why-brokers-see-a-global-opening-in-the-midmarket-565877.aspx