In the first of this three-part series, we identified six fundamental technology trends and explored how these will shape core technology architectures. Here we move on to explore how technology will also transform underwriting in each segment as carriers shift from binary models toward AI-enabled ‘bionic underwriting’ – where human

underwriting is augmented by advanced technologies in different ways.

Speed read

- Technology is automating and speeding up commercial insurance underwriting processes in ways that differ across SME, mid-market and large corporate segments.

- SME underwriting models need to combine automation rate, speed, and risk selection discipline, with use cases including algorithmic risk selection and pricing, and automated renewal triage.

- Mid-market underwriting, the natural home of bionic underwriting, will be reshaped by use cases such as automatically triaging incoming submissions, summarizing broker packs, and AI-driven portfolio analytics and pricing.

- Large corporate underwriting will not become ‘push button’, however frictions will be reduced by automating administration, using knowledge-platforms for cross-functional knowledge transfer, generating advanced risk insights from large datasets/unstructured information, and technology-assisted policy-wording review.

Successful insurers already calibrate their underwriting model to each segment, deploying underwriter talent where it adds the most value (e.g. complex accounts) and algorithms where these can handle routine decisions, thereby improving both precision and speed-to-quote across the portfolio.

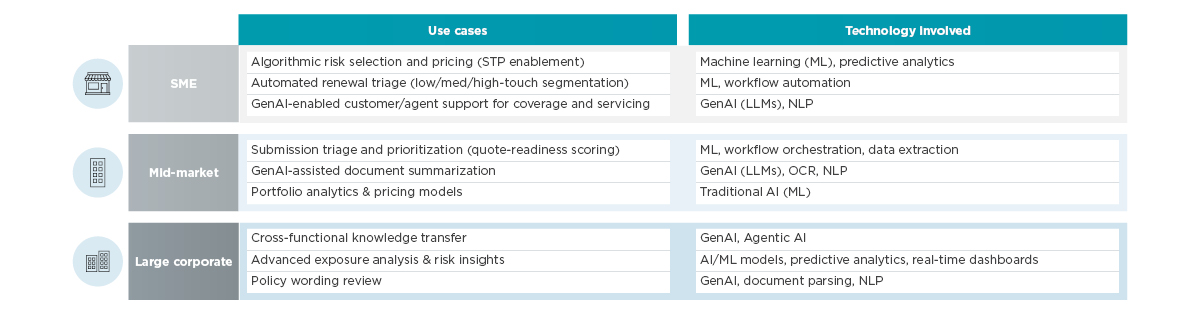

SME underwriting is characterized by maximum automation and speed, with algorithms handling the bulk of simple risks and humans intervening regarding exceptions. Large corporate underwriting sits at the opposite end, marked by bespoke, slow and expert-driven processes to capture unique risks. Mid-market underwriting balances the two – it requires more human analysis than in the SME segment but seeks greater efficiency than large account underwriting, e.g. through using data tools to assist underwriters and streamline simpler cases.

Technology will significantly change underwriting over the next five years, in ways that will continue to vary across each business segment. We expect that by 2035 manual pricing and underwriting will largely cease to exist for most personal and small commercial products, with automation exceeding 90% in simpler businesses. Large corporate insurance will remain less automated. However, even today 30–40% of underwriter time is often administrative, creating significant automation opportunities.

Below, we offer a series of use cases to characterize this transition in SME, mid-market, and large corporate segments. However, because the boundaries between these segments are fluid, the use cases may apply across multiple segments depending on the risk profile, product complexity and operating model.

SME

In this segment, the winning underwriting model needs to combine automation rate, speed, and risk selection discipline. High-impact underwriting use cases include:

- Algorithmic risk selection & pricing enables straight-through processing. Insurers are increasingly embedding AI models into the underwriting process to automatically select and price small business risks with minimal human intervention. By leveraging vast data (e.g. business attributes, loss history, third-party data), these algorithms instantly decide which submissions to accept or decline and at what price. Many small commercial carriers now achieve high straight-through processing rates, enabling quotes in minutes rather than days.

- Automated renewal triage. AI-driven renewal triage uses predictive analytics to segment policy renewals by risk and complexity, ensuring underwriters focus their work where it matters most. For example, machine learning models score renewing accounts on churn risk, value and likelihood of needing intervention. Low-risk, routine renewals can be auto-processed or given minimal touch, whereas medium-risk cases get some review and high-risk or high-value accounts receive full underwriting attention.

- GenAI-powered customer & broker assistance. Generative AI will increasingly be deployed as a 24/7 virtual assistant to help customers and brokers navigate insurance products and service their policies. Trained on policy wordings, guidelines and FAQs, these conversational agents can answer coverage questions, recommend appropriate coverage options, and even draft or explain policy documents in plain language. For instance, an AI chatbot might interact with a small business owner to determine their needs and suggest a tailored package of coverages, or guide a broker through underwriting guidelines and submission requirements.

Mid-market

Mid-market underwriting is the natural home of bionic underwriting: enough volume to justify automation, enough complexity to require expert judgment and negotiation. High-impact use cases include:

- Triage and prioritization (quote-ready scoring): AI can automatically read submissions incoming, via email or portal, and categorize or score them. Machine learning models use natural language processing (NLP) to extract key data from broker documents – e.g. insured name, industry, coverage requested, loss history – and then compare these against the insurer’s appetite and thresholds. This allows for quick filtering: straightforward in-appetite risks can be fast-tracked, while high-risk or non-standard cases are flagged for senior review or declined early.

An AI-powered triage system effectively routes the submission to the right desk or prioritizes it in an underwriter’s queue. The underwriter might see a dashboard of five new submissions assigned to them by an algorithm, already ranked by priority based on alignment with the portfolio strategy.

- GenAI-assisted document summarization of broker packs, loss runs, engineering reports: In mid-market commercial underwriting, brokers frequently submit complex and unstructured document packets. These might typically include broker proposals, multi-year loss runs and detailed engineering reports and require significant manual effort from underwriters to interpret, summarize and rekey into internal systems, slowing down triage and quote responsiveness.

A GenAI-powered document summarization assistant offers a transformative solution. Using large language models (LLMs), the system automatically extracts key information (e.g. limits requested, total insured values, prior losses), identifies inconsistencies or missing data, and generates a concise summary for the underwriter. It can also suggest follow-up questions or flag underwriting concerns based on the content. This data can be directly integrated into the underwriting workbench, significantly reducing administrative time while improving consistency and quote turnaround.

- Portfolio analytics & pricing models: Mid-market underwriting requires balancing speed and pricing discipline across diverse risks. AI-driven pricing models provide technical price indications based on historical losses and benchmarks, helping underwriters understand if a quoted price is below or above the model’s view and why.

AI-enabled portfolio analytics add another layer, flagging submissions that may create portfolio over-concentration by industry or region. For example, if the book is overweight in logistics within a CAT-prone area, the system can prompt a referral or capacity adjustment. This enables faster, more consistent underwriting decisions while steering the book toward a more profitable mix – essential in a high-volume, moderately complex environment like mid-market.

Large corporate

Large corporate underwriting will not become ‘push-button.’ The transformational goal is instead to remove friction, increase insight density, and shorten cycles without compromising control. To list a few high-impact use cases:

- Cross-functional knowledge transfer: In large corporate underwriting, complex risks often require rapid collaboration between underwriters, risk engineers and claims specialists. Yet, much of the institutional knowledge – prior deal context, emerging risk signals, engineering insights and claims precedents – remains undocumented or siloed across departments.

Knowledge transfer technologies – as offered by Swiss AI software company Starmind, for example – are becoming available to help resolve this problem and enable real-time expertise routing across the enterprise. When an underwriter encounters a complex exposure, such as turbine failure in a multinational energy risk, efficient knowledge transfer can instantly surface the most relevant claims handler, e.g. one that has dealt with a similar loss, or a risk engineer with operational insight on comparable infrastructure. This enables faster, more confident underwriting decisions, reduces duplicated investigation time, and ensures that lessons learned in one part of the organization are not lost in another. The result is improved underwriting accuracy, faster quote cycles and stronger knowledge retention across critical functions.

- Advanced exposure analysis & risk insights: AI/ML models can analyze large datasets and unstructured information to uncover insights that aid underwriting decisions. For instance, computer vision algorithms might analyze satellite imagery of large industrial sites to gauge property risks such as proximity to flood zones or areas vulnerable to brushfires. NLP techniques can read engineering reports or loss runs to identify common risk factors such as recurrent machinery breakdowns. GenAI can summarize lengthy Statements of Values (asset schedules) to highlight unusual exposures. Underwriters could also ask a GenAI assistant, “What are the top 5 loss drivers for this client based on past claims?” and get an instant synthesis from thousands of claim records.

These tools do not replace the underwriter’s own analysis, but they can significantly strengthen their situational awareness. Leading insurers are starting to use AI-driven digital platforms, often called ‘underwriting workbenches’, to bring together these kinds of analysis. For example, they may use them to aggregate internal data (claims, policy history) and external data (credit scores, geospatial risk indices) into one view.

- Policy-wording review: Crafting and reviewing contract wordings for a large corporate policy, which may run to 100+ pages, is a tedious task. GenAI language models are well-suited to assist here. An AI can compare a proposed wording against the company’s standard clauses to flag any deviations or non-standard endorsements, functioning as a smart checklist for compliance and coverage gaps. It can also suggest relevant clauses when underwriters draft manuscript endorsements.

For example, AI can pull from a library of pre-approved wording to address a specific exposure that the client needs covered. This assisted wording review speeds up the issuance process and reduces legal risk by catching problematic language. Some insurers are also experimenting with GenAI to generate draft policy summaries for brokers and clients, translating the legalese into plain language. While final review by human experts such as underwriters and lawyers remains essential, AI can reduce the cycles needed to get the wording right.

Underwriting process trends by segment – summary

Next steps to transform underwriting processes

Over the next five years, firms will need to industrialize bionic underwriting to accelerate quote-to-bind and improve decision quality. Executives should target reducing the administrative share of underwriter time and then expand transformation projects into analytics-driven insights and GenAI document intelligence.

Machine learning and GenAI are key technologies here, as our summary table above highlights. It is important to make data orchestration and AI governance ‘day one’ foundations. For example, EIOPA’s explicit expectations around explainability and human oversight mean governance must be designed in from the start. GenAI will not deliver sustained ROI without curated data, strong controls and integration into workflows.

The right executional mix will be needed to sustain transformation over the next five years, leveraging partners that can execute end-to-end, not just advise. Capco’s strength lies in combining core modernization, underwriting redesign, GenAI implementation and large-scale integration with deep domain expertise in insurer distribution, governance and change management. Read the third article in this series to explore how broker connectivity is about to be transformed.