Marc Oliver Berner | Published: 19 September 2019

The post-crisis mandatory change has undoubtedly affected banks in many ways. Indeed, banks have endured over a decade of continuous, complex and costly regulatory demands which has resulted, amongst many things, in a surge of digitization projects and the introduction of new technologies broadly covered by buzzwords like FinTech and RegTech.

However, the evolution of the regulatory environment also opens up significant opportunities for banking compliance to stay ahead of the game by making strategic changes to operating models and business processes through the introduction of a NextGen compliance function. NextGen compliance enables banks to deliver better service to their customers, implement regulatory change faster and, most importantly, reduce the overall cost and risk of their business activities.

In 2019, the regulatory tsunami is finally subsiding, and financial firms may be feeling that a well-deserved break is due. But is it really? In Switzerland, for instance, FIDLEG is just around the corner and, as outlined in our earlier blog, while many FIDLEG requirements echo MiFID II, it’s the subtle differences that are crucial for implementation.

This does not mean that another cumbersome regulatory project awaits Swiss banks in 2020. We believe that a detailed assessment (see FIDLEG health-check) carried out in parallel with questioning the current setup, will not only guarantee compliance but also maximize the investment in FIDLEG implementation and make NextGen compliance a reality.

NextGen compliance, also known as Compliance 2.0 or Compliance 2025, promises to revolutionize the compliance function. What is it and what does it mean for the financial services industry?

NextGen compliance is a technological component, but we also consider renewed and streamlined compliance processes an essential part of an updated compliance function. Smooth, intuitive processes and procedures save time and money. Technology comes into play where processes are repetitive or data-intensive. Computers outperform humans in analysing millions of data points, thus freeing their human colleagues to focus on the detailed and difficult tasks where artificial intelligence reaches its limits.

So, for Capco, NextGen compliance means a streamlined, technologically optimized and business-friendly compliance function which enables a bank to fulfil regulatory requirements as well as make smarter, faster and more profitable decisions backed by data.

As outlined in our previous blog, the MiFID II legacy processes often result in cumbersome compromises, due to an extremely inconsistent and unstable implementation in terms of the regulator input. With such a starting point, Swiss banks now need to implement FIDLEG, and on a tight budget.

We strongly believe that the decision of what to do with FIDLEG should be influenced by the possibilities offered by new regulatory technologies – RegTech. RegTech solutions not only ease the burden of regulatory compliance but also save money, very often paying off within the first two years.

The RegTech universe is evolving at a record-breaking speed, which makes it challenging for financial institutions to select the right partner for their purpose. An in-depth analysis of the current IT architecture and business model is necessary to identify the appropriate solution partner for long-term cooperation.

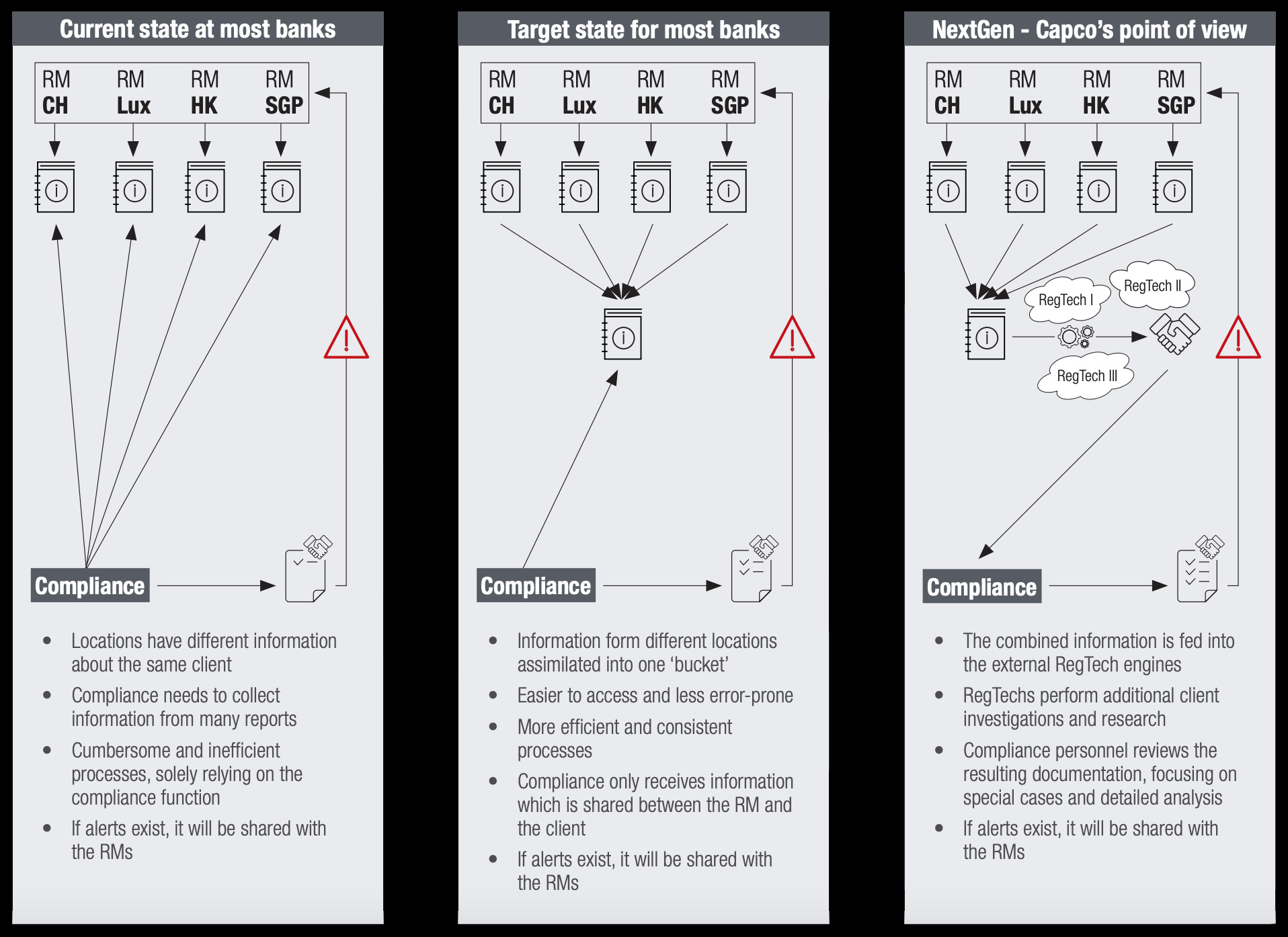

To illustrate NextGen compliance, let’s look at the Know Your Customer (KYC) and suitability & appropriateness requirements imposed through various regulations in the past few years.

For a Swiss bank, the suitability & appropriateness assessment translates into a key question - do we treat all clients under one regime or multiple regimes, based on their domicile? Taking just the E.U. and Swiss-based clients into account, banks already have to deal with MiFID II and FIDLEG where requirements are similar but not identical. So, does it make sense to have two regimes or not?

External vendors can accommodate setting up ‘rules’ based on client location, but it is also advisable to re-assess if the current business setup justifies multiple regimes. In other words, does an institution really need to keep all clients or would it be better off abandoning cross-border clients in exotic locations if the cost/income ratio is low?

To fully assess a client with all their accounts, locations and associated persons, quality input data is required, and this is where KYC requirements come into place. Often, different locations have different reporting formats and it is difficult to have a comprehensive view of a client based purely on the internal reports.

Centralizing client reports and streamlining processes are helpful steps, but to get a complete picture of a client, RegTech offers better solutions. We envisage a setup where internal data is enriched and evaluated by external vendors and fed back into the compliance function, which can then focus on special cases or detailed analysis. While onboarding a RegTech solution brings software and implementation costs, they can be offset by reduced manual workloads and significantly faster assessments. As mentioned earlier, RegTech solutions generally pay for themselves in the first two years of implementation.

FIDLEG is a great opportunity for Swiss banks to re-evaluate compliance. NexGen compliance functions are smaller, cheaper, more efficient and robust, and have the potential to provide immediate competitive advantage for banks.

Contact our RegTech and compliance experts to find out more about how to make your compliance function reach these goals.

Ingo Rauser

Partner

M +41 79 203 58 85

E ingo.rauser@capco.com

Schoaib Fazeli

Principal Consultant

M +41 79 833 72 02

E schoaib.fazeli@capco.com

Daniel Rubenov

Principal Consultant

M +41 79 135 85 41

E daniel.rubenov@capco.com

Marc Berner

Manager

M +41 79 135 85 21

E marc.oliver.berner@capco.com