Climate-related and environmental (C&E) risks are one of the ECB's key supervisory priorities for 2023-2025 as well as one of the main objectives of the EBA's Sustainable Finance Roadmap (2023-2025). As part of its priorities, the ECB defines concrete milestones and requirements until the end of 2024 particularly on the full integration of C&E risks into the Internal Capital Adequacy Assessment Process (ICAAP).

For supporting guidance, the ECB report on good practices for climate stress testing summarizes the identified good practices from the 2022 ECB Climate Stress Testing exercise to support banks on their transitional journey in C&E risk management with a focus on credit risk.1 Additionally, the report sheds light on the challenges faced by the banks in terms of climate risk scenario design, time horizons, modelling, scope of asset classes as well as data availability. Together with the good practices for C&E risk management2, the ECB also defines minimum standards to meet its 2023-2024 deadlines.

These deadlines require a high level of prioritization within banks to address implementation challenges in a timely manner as the transition planning and process will be monitored by supervisors, especially within the SSM via targeted deep dives, on-site inspections, SREP exercises or pillar 3 disclosures.3

Below we highlight the main priorities of the ECB and EBA roadmaps, the challenges banks face for the integration of C&E risks into their risk management and ICAAP as well as possible solution approaches.

The ECB sets the following three deadlines for 2023-2024 for the banks’ full integration of material exposures to climate related physical and transition risk drivers (C&E risks) into the overall bank (risk) management:4

The supervisory expectations in terms of strategy, risk management and governance are defined in the Guide on climate-related and environmental risks (September 2020).6 These expectations are accompanied by the good practices for C&E risk management (November 2022)2 and for climate stress testing (December 2022)1 to show exemplary implementations as well as benchmarks on how to meet the supervisory expectations for different business models and sizes in terms of proportionality.

Parallelly, the EBA published its roadmap on sustainable finance7 (December 2022), replacing the first EBA Sustainable Finance Action Plan (December 2019). The EBA has added new areas of interest including aspects related to sustainable product labelling, greenwashing, as well as prudential treatment of exposures in Pillar 1 and the enhanced risk supervision framework.

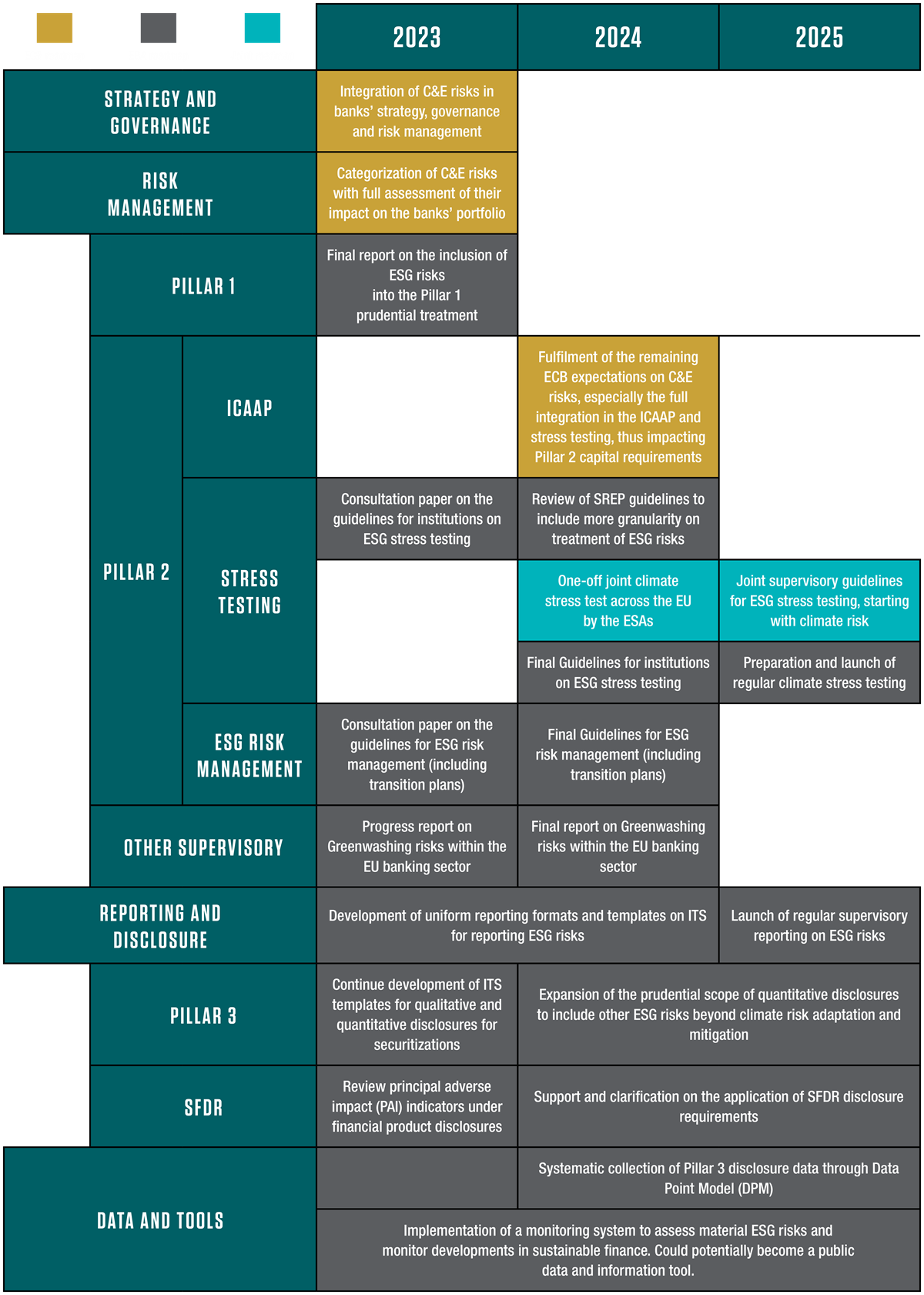

Figure 1 below shows a consolidated overview of the ECB and EBA roadmap until 2025, highlighting the key milestones to integrate C&E risks into strategy, governance and risk management encompassing the Three Pillars as well as the required data framework. The roadmap shows that the supervision concentrates at first on the expectation towards banks’ full integration of C&E risks into the Pillar 2 with the associated disclosure requirements.

Figure 1: ECB and EBA roadmap until 2025

The ECB 2022 climate stress test as a learning exercise showed that banks still earn around 60% of their interest income from business with non-financial customers in high carbon emitting industries and that around 60% of the participating banks had no internal climate stress testing framework at all (see also Capco’s thought leadership on this).8

To complement this observation, the results of the 2022 thematic review on C&E risks show that more than 80% of institutions conclude, based mainly on qualitative approaches, that physical and transition risks have a material impact on their risk profile in terms of credit (ca. 75%) and strategic (ca. 50%) risk mostly.9

Moreover, the thematic review reveals that over 85% of institutions have at least implemented basic practices for most of the areas addressed by the ECB in terms of identification of risk exposures, allocation of responsibilities, or setting initial KPIs and KRIs, but the institutions still lack methodological approaches and data availabilities to monitor and actively manage their portfolio and risk profile.

Thus, there is a high need to integrate and operationalize C&E risks in the risk management framework of banks, especially in their ICAAP, as drivers of the prudential risk categories and in consistency with their strategy and governance. For the stress testing framework, forward-looking factors over a long-time horizon are key for C&E risks to derive capital adequacy. This also implies that banks’ compliance with BCBS 239 (effective risk data aggregation, risk reporting, data quality management) requirements is further intensified to manage C&E risks adequately.

The materiality assessment of C&E risks, the enhancement of risk scenarios and time-horizons as well as the monitoring of the transition process of their clients are associated with huge data challenges in terms of macro and micro data (e. g. GHG emission, granular asset resolution and EPC rating data). For the full incorporation of C&E risks in the strategy, risk management and governance it is key to solve these data challenges.

The supervisory publications show clear priorities and minimum expectations (see thematic review2) supported by best practices for achieving full alignment by the end of 2024, especially for all institutions under the direct supervision of the ECB.

The ECB is going to closely monitor additional improvements and accordingly conduct on-site inspections for banks that fail to meet the deadlines to assist them in implementing solid remedial action plans. Nonetheless, the integration of C&E risks into financial institutions’ traditional risk management framework is still in its infancy with significant progress to be made on risk measurement and monitoring. Institutions need to begin operationalizing the C&E KRIs, sector policies, heatmaps and other risk identification metrics into the traditional risk monitoring processes to respond to regulatory pressure.

Against the background of the supervisory expectations, the integration of C&E risks requires a clear commitment by the management board and a structured as well as consistent approach for the implementation in strategy, risk, and governance with a forward-looking lens. To be effective, the implemented business strategy must be accompanied by intermediate targets, limits, and thresholds according to the risk appetite over the short to medium to long-term horizon.

Institutions must also be vigilant while adjusting their product offering and portfolio composition to ensure that the risk-mitigating instruments prevent misalignment with the institutions’ overarching sustainability objectives (for example, objectives agreed upon under NZBA commitments), especially for the most material risk exposures.

Such materiality assessment requires the need for granular data at the counterparty, facility or asset level and a data governance framework. A holistic data framework is crucial to avoid blind spots in the identification of C&E risks as was identified among 96% of institutions, of which 60% were major gaps9.

How Capco can help

Capco has a strong and rich track record of supporting clients with their change processes, spanning a wide range of business and regulatory requirements, process as well as data and IT implementations. We have developed a unique integration approach to C&E risks into the risk management processes and creating a robust data and IT framework. Contact us to learn more about how we can help your institution on its journey to change and give you an edge over your competition.

1 See ECB report on good practices for climate stress testing (europa.eu)

2 See Good practices for climate-related and environmental risk management (europa.eu)

3 See ECB Banking Supervision: SSM supervisory priorities for 2023-2025 (europa.eu)

4 See ECB sets deadlines for banks to deal with climate risks (europa.eu)

5 See Guide on climate-related and environmental risks (europa.eu)

6 See Guide on climate-related and environmental risks (europa.eu)

7 See EBA Roadmap on Sustainable Finance.pdf (europa.eu)

8 See https://www.capco.com/Intelligence/Capco-Intelligence/ECBs-2022-Climate-Stress-Test

9 See www.bankingsupervision.europa.eu/ecb/pub/pdf/ssm.thematicreviewcerreport112022~2eb322a79c.en.pdf